Many UK businesses assume that only successful projects can qualify for R&D tax relief. In reality, HMRC does not assess an R&D claim based on whether a project achieved its intended outcome or was commercially successful. What matters is whether the project sought to resolve scientific or technological uncertainty through a systematic process. Many qualifying R&D projects involve approaches that fail, are abandoned or prove technically unworkable. Where those activities were undertaken to resolve scientific or technological uncertainty, they may still qualify for R&D tax relief.

This article explores common examples of failed R&D approaches that may still qualify for R&D tax relief, together with examples that would not meet HMRC’s eligibility criteria.

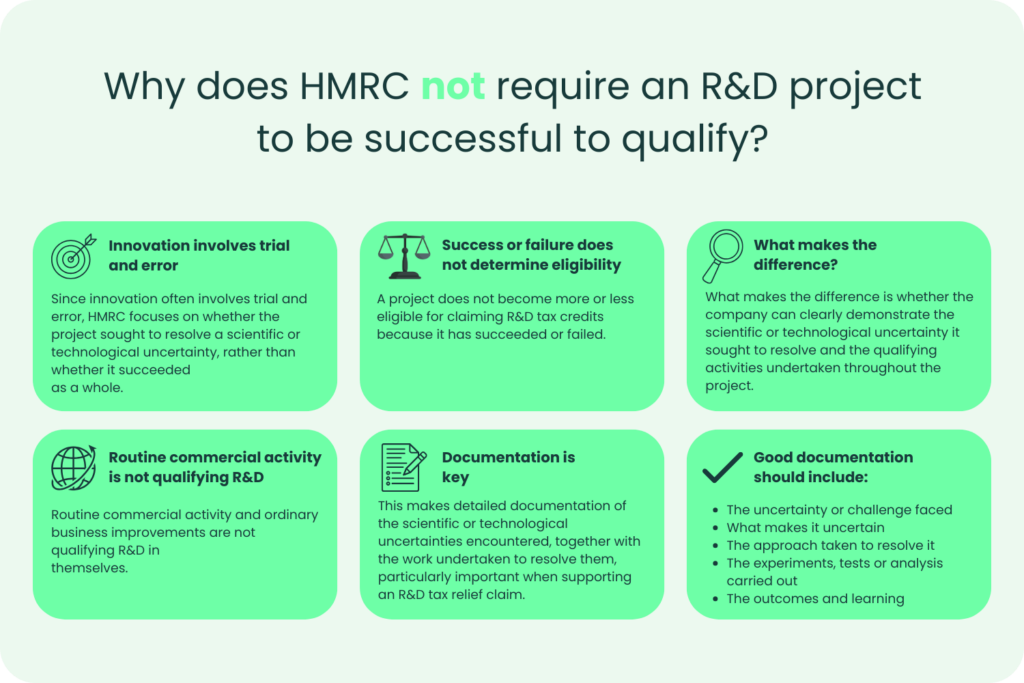

Why does HMRC not require an R&D project to be successful to qualify?

HMRC does not require an R&D project to be successful in order for it to qualify under the R&D tax relief criteria. Since innovation often involves trial and error, HMRC focuses on whether the project sought to resolve scientific or technological uncertainty, rather than whether it ultimately succeeded. A project does not become more or less eligible because it has succeeded or failed. What will make the difference is whether the company can clearly demonstrate the scientific or technological uncertainty it sought to resolve and the qualifying activities undertaken throughout the project.

Routine commercial activity and ordinary business improvements are not qualifying R&D in themselves. This makes detailed documentation of the scientific or technological uncertainties encountered, together with the work undertaken to resolve them, particularly important when supporting an R&D tax relief claim.

What counts as a scientific or technological uncertainty?

A scientific or technological uncertainty exists where the knowledge or method needed to achieve the advance is not readily deducible by a competent professional working in the relevant field.

Examples of sectors where qualifying R&D may arise include:

- Software development

- System integration

- Manufacturing and materials

- Pharmaceuticals and life sciences

- Electronics and hardware

- Food and drinks

What are some examples of failed R&D approaches that still qualify?

An unsuccessful outcome does not prevent a project from qualifying for R&D tax relief. HMRC considers whether the project sought to resolve scientific or technological uncertainty, rather than whether it resulted in a commercially successful product or process.

Qualifying expenditure may include work undertaken during unsuccessful experimentation, abandoned prototypes and testing that demonstrated a proposed solution would not achieve the intended outcome. Examples of failed or abandoned approaches that may still qualify include:

Scrapped prototypes

A prototype does not need to be completed in order to support a R&D tax credit claim. If the prototype was developed as a possible solution to a scientific or technological uncertainty, the activities undertaken may still constitute qualifying R&D activities. This includes abandoned prototypes as testing showed the proposed approach could not achieve the required result.

Failed material systems

Developing a new product or improving an existing system often requires testing multiple avenues before determining whether any approach could achieve the required technological outcome.

Where those experiments were undertaken to resolve scientific or technological uncertainty, unsuccessful projects may still constitute qualifying R&D activities.

Dead-end software algorithms

Software development frequently involves exploring algorithms that ultimately prove unsuitable. If developers were attempting to resolve a technological uncertainty that could not readily be overcome by a competent professional, the unsuccessful development work may still qualify.

Unsuccessful clinical or laboratory testing

Research projects within life sciences often involve experiments that do not produce the expected outcome. Failed laboratory work or clinical testing can still qualify where the activity sought to advance science or technology by addressing genuine scientific or technological uncertainty.

To support an R&D tax relief claim, businesses should document the scientific or technological baseline, the uncertainties encountered and the work undertaken to resolve them.

What are some examples of failed R&D approaches that do not qualify?

There are some examples of failed R&D approaches that will not meet the qualifying criteria for claiming research and development tax credits. Examples include:

- Projects that were abandoned due to insufficient funds.

- Products or services that failed due to a lack of customer demand.

- A website redesign using standard development techniques and software.

- Replacing existing equipment with newer commercially available equipment, without resolving scientific or technological uncertainty.

- An unsuccessful marketing campaign.

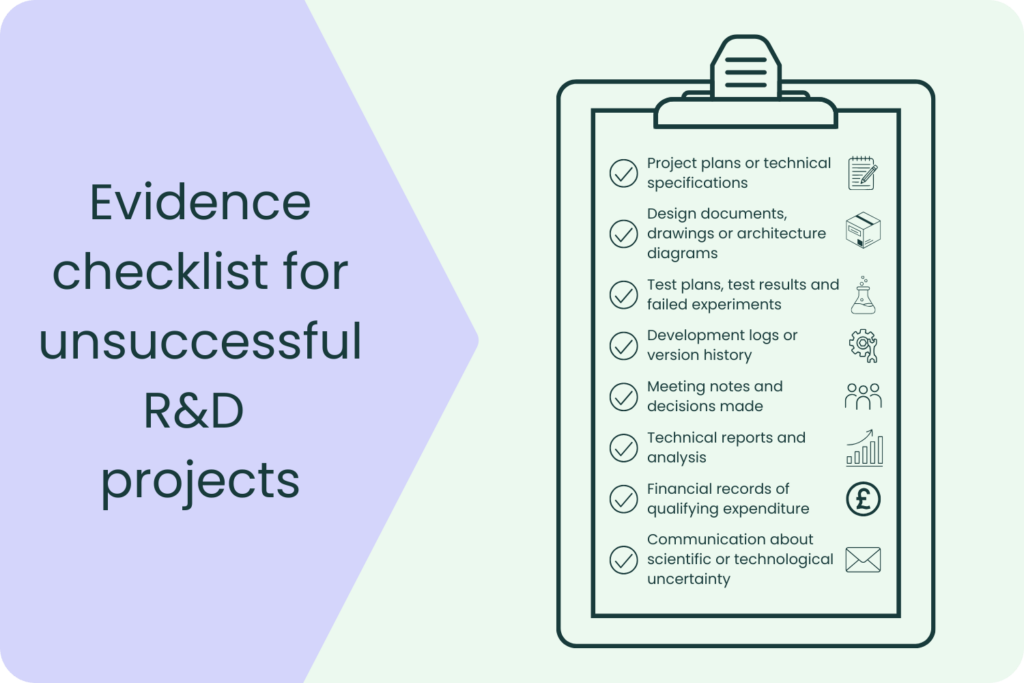

What evidence should you keep for an unsuccessful R&D project?

When a business claims R&D tax relief, the work undertaken to resolve the scientific or technological uncertainty is more important than the outcome of the project.

Whether the project was abandoned or it was unsuccessful, the business should retain records that clearly demonstrate the qualifying research and development activities that were carried out and the decisions made throughout the project.

There is a variety of different ways to evidence information, such as:

- Project plans or technical specifications which outline the intended objectives.

- Design documents, engineering drawings or software architecture diagrams.

- Test plans, test results and any records of failed experiments.

- Development logs, history of different project versions or laboratory notebooks showing how the work progressed.

- Meeting notes that clearly outline all technical discussions, challenges and decisions.

- Clear evidence explaining any approaches that failed or were abandoned.

- Records of the competent professionals who had any involvement and the technical uncertainties they aimed to resolve.

- Financial records linking qualifying expenditure to the relevant R&D activities.

The aim is to demonstrate that the project involved a systematic attempt to overcome scientific or technological uncertainty. A failed result doesn’t weaken a claim if the qualifying work can be evidenced. Maintaining clear records also makes it easier to prepare a well-supported technical narrative. It also provides the business with the necessary support when responding to questions HMRC may raise during the compliance process.

What are some common misconceptions about failed R&D projects?

Some misconceptions have led UK businesses to overlook their qualifying R&D work simply because that project did not achieve a successful outcome.

Below are some of the most common misconceptions we hear when speaking with businesses about unsuccessful R&D projects:

“A failed project can’t qualify for R&D tax relief.”

One of the most common misunderstandings is that an R&D project must be successful to qualify for R&D tax relief. In practice, HMRC does not require a project to succeed. The key consideration is whether the company undertook qualifying R&D activities to resolve scientific or technological uncertainty.

“Only products that reach the market qualify.”

A commercial launch is not part of the eligibility criteria. A project may qualify even if development stopped before production or the final product was never sold, provided the qualifying R&D activities meet the definition set by HMRC.

“Abandoned projects are automatically excluded.”

Projects are often discontinued because testing demonstrates that a proposed solution is technically unworkable or another way of approaching a solution is required. Work that was carried out before the project was abandoned may still qualify where there is evidence that the work sought to achieve a scientific or technological advance.

“Patents are required to support an R&D claim.”

Patentable inventions and qualifying R&D are not the same. Many companies undertake eligible R&D without applying for a patent, while some patented products may contain little or no qualifying R&D. Eligibility will depend on the scientific or technological uncertainties addressed rather than whether the intellectual property protection had been sought.

What should businesses remember about failed R&D projects?

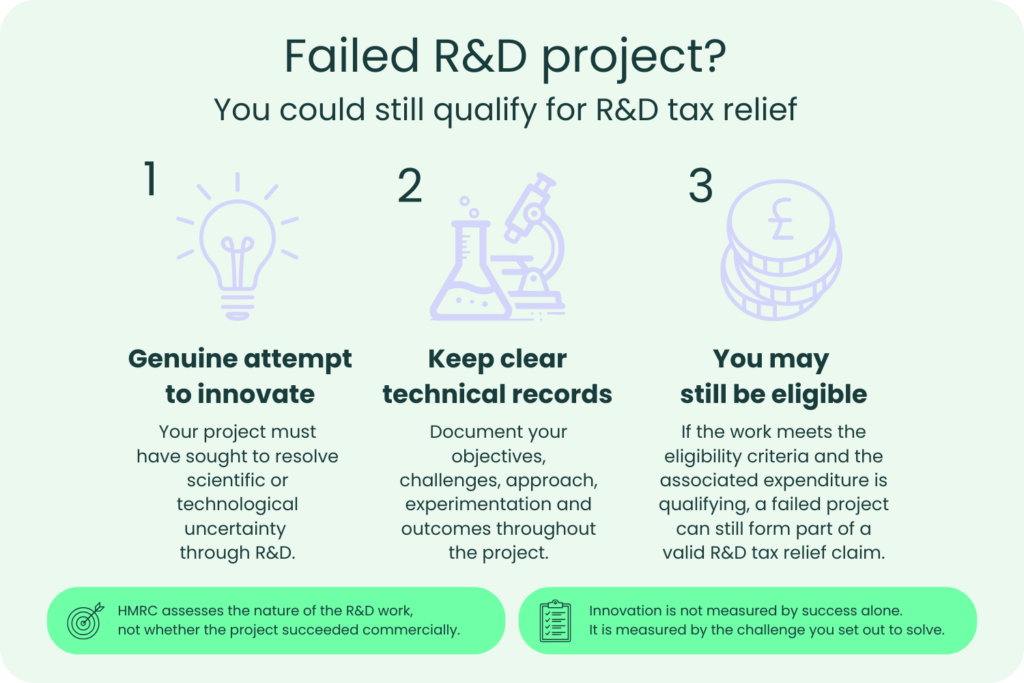

Many businesses assume a failed project cannot qualify for R&D tax relief. In practice, unsuccessful outcomes are common within genuine research and development. HMRC is interested in whether the project attempted to resolve scientific or technological uncertainty, not whether the work resulted in a commercially successful product or process.

Keeping clear technical records throughout a project makes it much easier to demonstrate the qualifying activities undertaken. If the work meets the eligibility criteria and the associated expenditure is qualifying, a failed project may still form part of a valid R&D tax relief claim.

Closing thoughts

At Alexander Clifford, we work with UK businesses to identify qualifying R&D activities, assess whether the activities and expenditure meet the qualifying criteria, and prepare evidence-led R&D tax relief claims that align with HMRC’s guidance.

One of the most common misconceptions we encounter is that unsuccessful projects cannot qualify for R&D tax relief. In reality, many valid R&D tax credit claims include projects where prototypes were abandoned, scientific or technological approaches failed or the intended outcome was never achieved. The main consideration is whether the work sought to resolve scientific or technological uncertainty through qualifying R&D activities.

Understanding where a failed project meets the eligibility criteria for R&D tax credits can make a material difference to the value of a claim. By reviewing the project objectives, the scientific or technological uncertainties encountered, and the activities undertaken to address them, businesses can ensure that qualifying activities are recognised, regardless of the final outcome.

If you’re unsure whether unsuccessful or abandoned projects could form part of an R&D tax relief claim, our financial and technical teams will assess your activities and explain the evidence required to support a compliant submission.

For more information regarding failed R&D projects and claiming R&D tax relief, please get in touch with our team.