Since the introduction of the Additional Information Form (AIF) in August 2023, HMRC has collected structured information about R&D claims to improve compliance, reduce error and fraud, and support the risk assessment stage.

In this article, we are going to be discussing what the AIF is, why it was brought in and the importance of completing an Additional Information Form during the R&D claim process.

What is an Additional Information Form?

The Additional Information Form, also known as the AIF, is a digital form which gathers structured information about qualifying R&D activities that are included within an R&D tax relief claim.

The company must provide the following R&D project information:

- Qualifying expenditure

- The technical projects undertaken

- The parties involved in compiling the claim

The form is a mandatory step in the R&D claim process and it must be submitted before the Company Tax Return, which is also referred to as the CT600.

Why was the Additional Information Form introduced?

The Additional Information Form (AIF) was brought in by HMRC to improve the quality of Research and Development tax relief claims, reduce inaccurate submissions and provide all information required to assess R&D claims more efficiently.

By collecting structured information at the point of submission, HMRC can carry out more effective risk assessments and identify claims that may require further review.

Companies must clearly outline their technical narrative and qualifying expenditure so HMRC can assess the claim more effectively.

What does the Additional Information Form require?

The Additional Information Form requires a range of information that detail the exact scope of an R&D tax credit claim. Below we have provided a brief list of what businesses need to complete a compliant Additional Information Form:

- Company details such as the UTR, PAYE reference, VAT registration and SIC code.

- Project details such as a technical explanation of the R&D undertaken. You must describe what scientific or technological advance that the business is aiming to achieve and any scientific or technological uncertainties that were faced during the project’s timeline.

- A structured breakdown of qualifying R&D expenditure such as staffing, software, consumables and subcontractors.

- Details of the senior management, R&D advisers and any other R&D agents involved in the project’s development.

What are the key Additional Information Form submission rules?

There are some key rules when it comes to the submission stage for the Additional Information Form. According to the HMRC guidelines, these rules are:

Mandatory submission

If the Additional Information Form is missing from the claim, submitted after the deadline or submitted after the CT600, HMRC will automatically reject the R&D claim.

Accounting periods

If a business is claiming R&D tax relief for more than one accounting period, they will need to submit a separate Additional Information Form for each period.

Online only

An AIF can only be completed online using the government’s services; there is no paper version available.

How does HMRC use the information provided in the AIF?

HMRC uses the information provided in the Additional Information Form to perform risk profiling, assess claims against the legislative requirements and identify submissions that may require further compliance checks.

As the AIF was brought in to streamline the process of an R&D tax credit claim, this verification process will hold claimants accountable and reduce risks of error and fraud.

From tracking accountability to verifying administrative requirements, there are different ways that HMRC uses the structured data gathered from the Additional Information Form. Other areas HMRC focuses on include:

- Assessing claim validity

- Performing risk assessments

- Filtering for enquiries

- Tracking accountability

- Validating administration

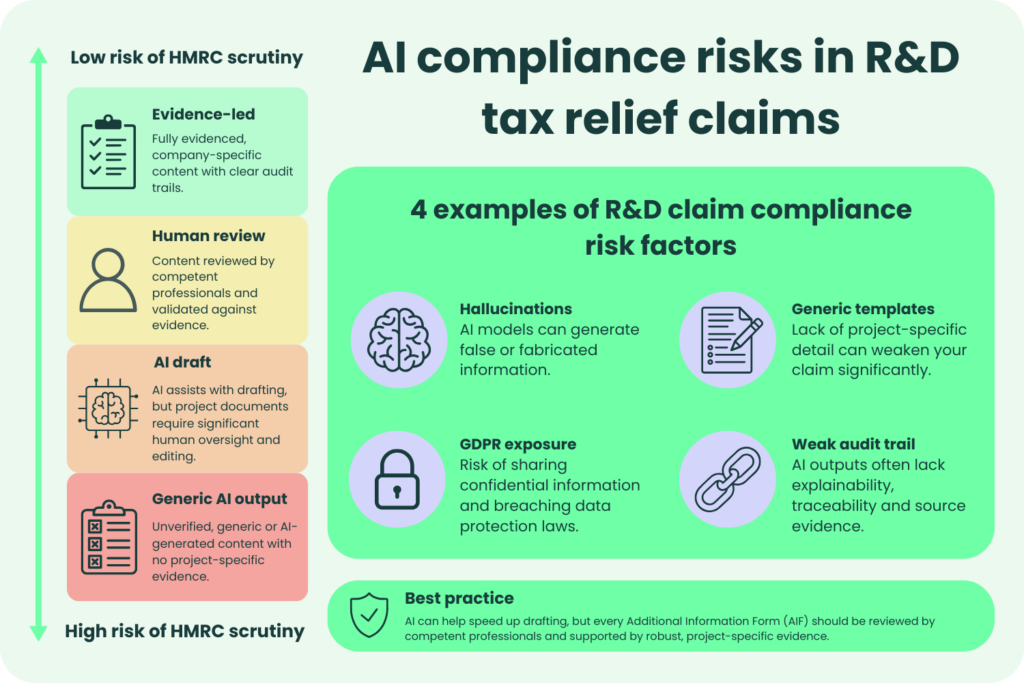

How can AI-generated AIF submissions create compliance risks?

AI is increasingly becoming more accessible to businesses across the nation, however if used incorrectly, businesses could face enquiries being opened by HMRC.

Using AI to complete an Additional Information Form can create compliance risks if it generates false or inaccurate information or if confidential data is shared with AI tools without the appropriate GDPR safeguards.

There are specific risks associated with using AI when conducting an Additional Information Form, these include:

Data factual errors

AI models can create untraceable details, false studies and incorrect statistics. Submitting project documentation as factual information can result in rejected claims. However, where inaccuracies are careless or deliberate, penalties may apply.

Potential GDPR and confidentiality risks

The use of public AI tools to draft an Additional Information Form may involve sharing confidential project information with an external AI service provider.

If appropriate safeguards are not in place, this could result in creating serious risks under the UK GDPR and the Data Protection Act 2018, especially when personal data has been processed without lawful authorisation or adequate security measures have been put in place.

Businesses should ensure that all confidential project information is protected and that any AI tools used comply with their data protection obligations.

Using a generic AI template

Generic templates created using artificial intelligence can create risks due to the lack of authentication and business-specific detail. An Additional Information Form must accurately reflect the company’s qualifying activities, scientific or technological uncertainties and eligible expenditure.

Generic AI-generated content may include:

- Inaccurate assumptions

- Incorrect key project information

- Failure in demonstrating how the R&D activity has met HMRC’s criteria

This content will risk weakening the credibility of an R&D claim and increase the likelihood of HMRC raising questions or requesting further project evidence.

Loss of audit trails and explainability

Businesses are increasingly expected to maintain clear audit trails that support the information included within an R&D claim. Standard AI systems often provide outputs without a suitable explanation of how conclusions were reached. Therefore, it can be difficult to demonstrate transparency, validate decisions or comply with laws and regulations.

How would an AIF be prepared before beginning the R&D claim process?

The Additional Information Form must be prepared with caution and accuracy. The information inputted into this digital form will be included in the company’s R&D tax relief claim and may be used by HMRC to assess the claim as part of the compliance process.

Although the AIF is submitted when making an R&D tax relief claim, much of the information required should be gathered before the claim is prepared.

Maintaining accurate records throughout the accounting period makes it easier to complete the form and helps ensure the information submitted is consistent and supported by authentic evidence.

Before preparing R&D tax relief claims, businesses should identify the projects that contain activities that may qualify for R&D tax credits. This includes establishing the scientific or technological advance being sought, the scientific or technological uncertainties encountered and the work undertaken by competent professionals to resolve the uncertainties.

Financial records should also be reviewed to identify eligible R&D expenditure. This may include staffing costs, externally provided workers, software, consumables and subcontracted R&D where these meet the relevant legislative requirements. Reconciling these costs before preparing the claim can reduce the risk of inconsistencies between the Additional Information Form and the Company Tax Return.

It’s also good practice to gather supporting evidence as the project progresses.

Examples include:

- Design documents

- Technical meeting notes

- Testing records

- Development logs

All of these examples can help demonstrate that qualifying R&D activities took place if HMRC requests further information during a compliance check.

The Additional Information Form requires details of the competent professionals responsible for the technical work, as well as any advisers or agents who assisted with compiling the claim submission. Having this information available before drafting the claim can help avoid delays and reduce the likelihood of errors.

What is the best practice for completing an Additional Information Form?

The best practice for completing an Additional Information Form is to submit it before the Company Tax Return is filed, this can also be on the same day. Submitting the CT600 first will result in HMRC automatically rejecting the claim.

There are several best practices businesses can follow to complete an Additional Information Form in line with HMRC’s requirements. These may be:

Submit the claim through the Corporation Tax Government Gateway

File the Additional Information Form via your company’s Corporation Tax Government Gateway account. A separate AIF must be completed for each accounting period included in the claim.

Prepare clear technical narratives

Avoid marketing or commercial language. Instead, explain the scientific or technological baseline at the outset of the project, the advance the company sought to achieve, the scientific or technological uncertainties encountered, and the systematic work undertaken to resolve them.

Reconcile the financial information

Check that the total qualifying expenditure reported in the AIF matches the figures included within the Corporation Tax return and supporting evidence of R&D activity. Be prepared to allocate costs across HMRC’s expenditure categories, including staffing costs, consumable items, software, subcontracted R&D, and externally provided workers where applicable.

Disclose responsibility and adviser details

Identify those responsible for the project work such as a director, who will accept responsibility for the accuracy of the claim. If an external adviser or agent assisted with the claim, their details must also be disclosed.

Closing thoughts

At Alexander Clifford, we help UK businesses prepare evidence-led R&D tax relief claims that reflect HMRC’s expectations and the legislative requirements.

As part of the claiming process, we ensure that the Additional Information Form (AIF) accurately explains the scientific or technological advances sought, the uncertainties encountered and the qualifying R&D activities undertaken.

The introduction of the AIF reflects HMRC’s focus on improving the quality of R&D tax relief claims and gaining a better understanding of the projects. The information provided helps HMRC assess compliance risks and distinguish genuine R&D from routine commercial activity. A well-prepared AIF should present a clear and factual explanation of the work carried out, supported by appropriate technical and financial evidence.

Understanding what HMRC expects from an AIF can help businesses prepare better supported R&D tax relief claims. Taking each step with caution to explain projects clearly and consistently is an important part of demonstrating that the qualifying criteria have been met.

Want to ensure your Additional Information Form accurately reflects your qualifying activities? Look no further because our financial and technical teams can help review your projects and prepare a compliant submission.

If you have been seeking a trusted R&D tax adviser to guide you through the Additional Information Form process or preparing an evidence-led R&D tax relief claim, please get in touch today.