Contemporaneous documentation is one of the most crucial areas of a compliant R&D tax relief claim. Rather than relying on estimates or post-project recollections, maintaining contemporaneous documentation will create a clear audit trail of the work undertaken, the uncertainties faced, the decisions made by competent professionals and the resources devoted to resolving those challenges.

In this article, we are going to be discussing the importance of contemporaneous documentation in R&D tax credit claims.

What counts as contemporaneous documentation?

Contemporaneous evidence refers to documentation such as:

- Progress reports

- Meeting notes

- General notes

- Site diaries

- Audit trails

- Financial reports or transactions

These are only some of the many forms of suitable contemporaneous documentation that may help evidence qualifying R&D activities and expenditure.

Why does contemporaneous documentation have to be in real time?

Contemporaneous documentation must be completed in real time or immediately afterwards an activity has taken place to avoid bias and gaps within the progress of the project. Real-time records capture the progress of the project in an honest and credible manner before any personnel changes or the scientific or technological rationale behind key decisions is lost. This creates a stronger evidential record when demonstrating scientific or technological uncertainties and the activities undertaken to resolve them.

How does contemporaneous documentation support an HMRC enquiry?

When HMRC reviews an R&D tax relief claim, they will typically look for evidence that supports the financial and technical aspects of the project. Having contemporaneous documentation will provide justifiable project records that demonstrates how the work evolved alongside what scientific or technological uncertainties were encountered and the steps taken to resolve them.

Where retrospective accounts are prepared later when the project is nearly completed or after completion, contemporaneous records will reflect in real-time what was known at the time when the activities were undertaken. This helps establish the project’s baseline knowledge, explain why the solution was not readily deducible by a competent professional and provide evidence of the expenditure included within the claim.

Strong contemporaneous evidence can also help businesses respond more efficiently to HMRC enquiries. Where project decisions, testing activities, meeting discussions and expenditure records have been documented throughout the project lifecycle, it is often easier to demonstrate that the claim has been prepared on a reasonable and evidence-based foundation.

Does HMRC require contemporaneous documentation?

HMRC does not expect a specific type or format of contemporaneous documentation to be used when claiming for R&D tax relief. There is no requirement to maintain a particular template, project log or record-keeping system.

What HMRC does require under general Corporation Tax Self-Assessment rules is that businesses must maintain sufficient, credible records to demonstrate how they arrived at both the technical and financial aspects of their claim submission.

In practice, maintaining documentation throughout the lifecycle of a research and development project is one of the most effective ways of evidencing qualifying R&D activities and expenditure.

Real-time records are often the strongest way to substantiate:

- The scientific or technological uncertainties encountered

- The systematic trials or work carried out to resolve them

- The active involvement and decisions of competent professionals

- How project directions and technical boundaries evolved

- The exact methodology used to calculate qualifying expenditure

Where contemporaneous evidence is unavailable, businesses may still be able to support an R&D claim using other records and testimony from employees involved in the project. This can be more difficult to authenticate, particularly where significant time has passed since the work was completed.

For this reason, R&D tax advisers and HMRC enquiry teams recommend contemporaneous documentation as good practice. It makes it much easier to support an R&D tax relief claim if HMRC requests further information later down the line.

What are the risks of not maintaining contemporaneous documentation?

Many businesses only begin gathering evidence when it’s time to prepare for their R&D tax relief claim. By that stage, key project details may have been forgotten, employees may have left the business and supporting records may no longer be available.

This can create significant difficulties when explaining the scientific or technological uncertainties encountered during the project and can increase reliance on estimates or assumptions. In certain situations, lack of qualifying evidence may result in qualifying activities or expenditure being excluded from the claim.

How much contemporaneous evidence is enough for an R&D claim?

To put it simply, there is no specific threshold for the amount of contemporaneous evidence for an R&D claim. HMRC requires sufficient records to support the technical and financial basis of the claim.

Evidence should include:

- Technical eligibility

- Financial accuracy

The claimant company must be able to provide detailed project descriptions and should retain them to support the information submitted through the Additional Information Form which is a mandatory requirement.

What are the most common documentation mistakes identified by HMRC?

When it comes to common mistakes, HMRC frequently identifies gaps in project records, missing supporting evidence and inconsistencies between technical and financial documentation. These shortcomings can weaken the evidential basis of a claim and increase the likelihood of further scrutiny from HMRC.

Common issues identified during HMRC enquiries include:

- Documenting the commercial features and project milestones of a product, rather than focusing on certain scientific or technological uncertainties that were faced.

- Failing to retain original development records, technical logs or sprint data, resulting in R&D activities that cannot be properly evidenced.

- Maintaining records with gaps, missing details or rounded time estimates that fail to prove exactly how much time employees spent on qualifying R&D work.

- Discrepancies between the figures submitted on the mandatory Additional Information Form (AIF), financial records and the final tax return creates uncertainty over the accuracy of reported figures.

- Incorrectly categorising R&D expenditure, such as confusing independent subcontractors with externally provided workers, resulting in costs being allocated to the wrong area of the claim calculation.

- Treating routine business problems or standard software debugging as an R&D advancement, even though the solution could have been easily figured out by a competent professional using available knowledge or methods.

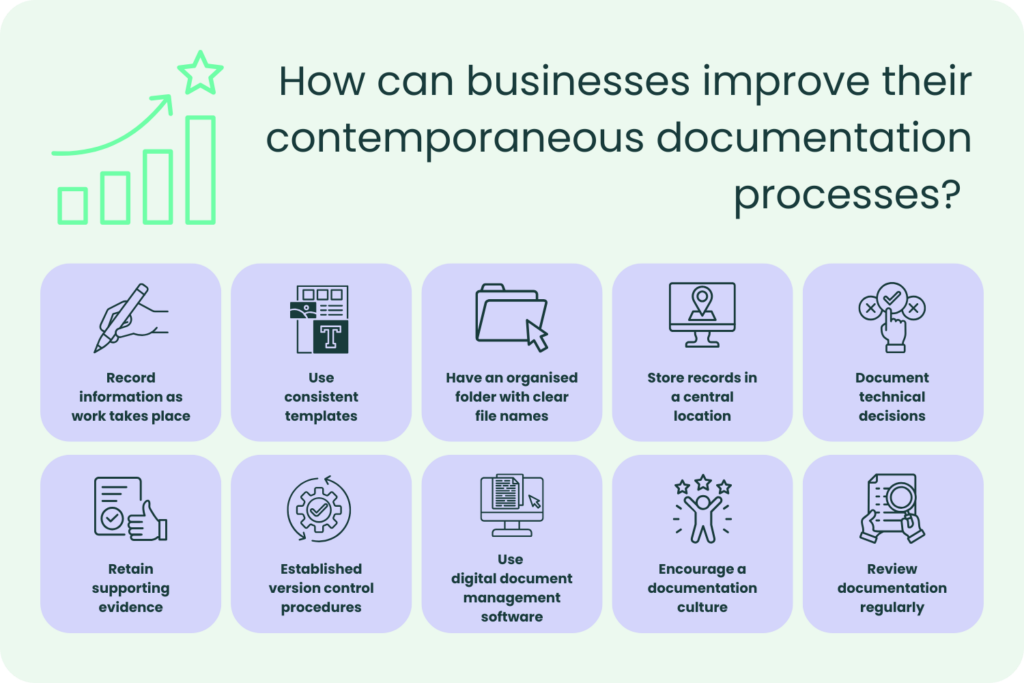

How can businesses improve their contemporaneous documentation processes?

Businesses can improve their contemporaneous documentation processes by maintaining records throughout the project lifecycle rather than attempting to recreate events at the point of claim preparation. Using standard templates, recording key technical decisions as they occur and storing project information in a central location can help create a clear and consistent audit trail.

Regularly documenting scientific or technological uncertainties, testing activities and project outcomes also makes it easier to demonstrate qualifying R&D activities and support a claim if HMRC requests further information.

Record information as work takes place

Creating project records while the work is actually taking place, rather than relying solely on estimates or memory, will ensure that financial and technical data remains accurate.

Use consistent templates

Implement consistent templates for project updates, meeting notes and technical reports. Keeping documentation in a consistent format improves the quality of the records and makes it much easier for HMRC to review.

Document technical decisions

Record key project developments, technical challenges and decision-making processes throughout the project lifecycle to support the technical narrative of an R&D claim.

Retain supporting evidence

Retain copies of supporting evidence such as project plans, testing records, meeting minutes, timesheets, invoices and other relevant documentation which was made at the same time the R&D activities took place.

Established version control procedures

Maintain the history of your project documents and any design changes undertaken to demonstrate how the research and development evolved over time and identify those responsible for key decisions.

Store records in an organised system

Keeping technical and financial documentation within an organised system with clear file names creates a clear audit trail and reduces the risk of critical information being misplaced.

Use digital document management software

Digital document management systems and time-tracking software are two examples of what can help businesses automatically maintain accurate records and support claim preparation.

Encourage a documentation culture

Ensure employees understand the importance of recording qualifying activities, scientific or technological uncertainties and project outcomes throughout the ordinary course of their work.

Review documentation regularly

Periodically assess project records to identify any gaps in evidence early on, well before preparing an R&D tax relief claim.

Closing thoughts

At Alexander Clifford, our team works with companies across the nation to identify qualifying R&D activities, assess technical eligibility and develop evidence that aligns with HMRC’s expectations when it comes to submitting an R&D tax credits claim.

Contemporaneous documentation plays an important role in demonstrating that qualifying R&D took place. Project records, technical reports, test results and decision-making evidence can all help support the narrative of a claim and provide context around the scientific or technological uncertainties encountered during a project.

A well-supported claim is not simply about documenting successful outcomes. It should show the process undertaken to seek an advance in science or technology, the uncertainties faced and the work carried out in an attempt to resolve them.

Maintaining project records throughout the lifecycle of a project makes the claiming process more straightforward and allows businesses and R&D tax credit advisors to prepare accurate and evidence-led submissions.

If you would like to discuss more about the requirements of submitting contemporaneous documentation and to seek the potential of claiming R&D tax relief for your business, please get in touch with our team.