HMRC has introduced a reform to UK R&D tax relief, merging the two current R&D tax credit schemes – R&D SME and RDEC. This affects claims for accounting periods beginning on or after 1 April 2024.

Under this R&D combined scheme, you could get an expenditure credit rate of 20% (net c. 15%–16.2% depending on your CT rate).

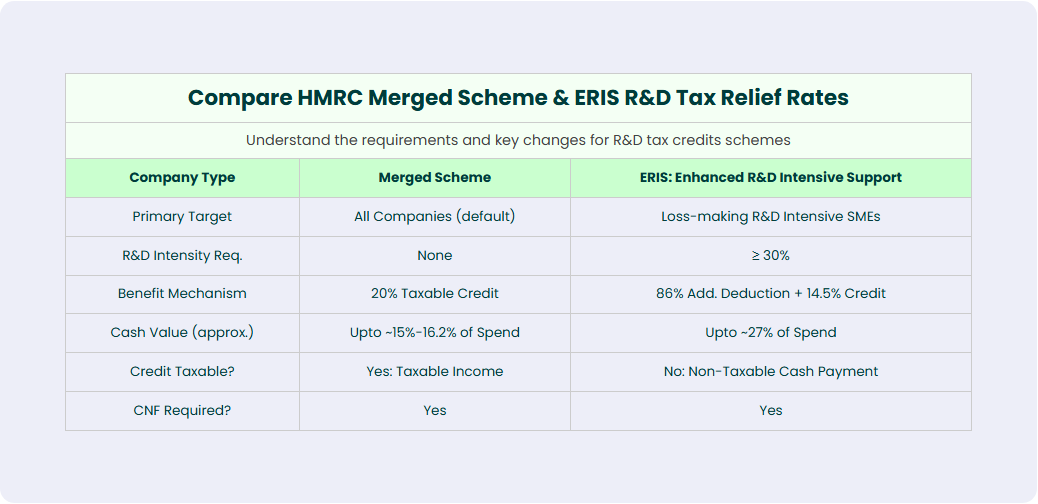

The new R&D merged scheme runs alongside the Enhanced R&D Intensive Scheme (ERIS), rewarding research and development-intensive businesses for contributions towards technological advancement and innovation.

Important:

The R&D Merged Scheme applies to accounting periods starting on or after 1 April 2024. Your switch date depends on your company’s financial year-end.

What is the New Merged R&D Tax Credit Scheme in the UK?

The merged scheme has unified the existing SME and RDEC tax credit schemes into one streamlined and consistent system.

While bringing together the two incentive schemes, HMRC has retained most of the existing RDEC structure and incorporated benefits from the SME scheme.

All businesses that meet qualifying research and development projects can now benefit from standardised above-the-line credit like the original RDEC scheme.

This merged research and development scheme makes the tax relief visible in a company’s profit and loss account, and offers greater transparency for financial planning.

By merging the schemes, HMRC aims to remove unnecessary complexity, reduce the risk of fraudulent claims, and provide businesses with greater certainty when planning R&D projects.

When Does the Merged R&D Scheme Apply?

The merged R&D expenditure scheme is now well underway.

Legislated in the Autumn Statement of 2023, the scheme has now come into effect for accounting periods on or after 1 April 2024.

The merger brought in an equal rate for all businesses making an R&D tax credit claim. This updated rate allows claimants to more easily calculate their claim.

What is the Core Eligibility Criteria for the Merged Scheme?

To qualify for the R&D Merged Scheme, a company must:

- Be a UK-registered business subject to Corporation Tax

- Undertake R&D that meets the CIRD81900 definition of a qualifying project

- Demonstrate commercial purpose, ownership of risk, and control over the work

What Rates Can I Claim from the Merged R&D Scheme?

The new R&D merged scheme rates offer a 20% gross expenditure credit for qualifying expenditure to all R&D companies, regardless of size, industry or project type.

The expenditure credit is treated as taxable income. Therefore, the net benefit after corporation tax ranges from 15% to 16.2% depending on the type of Corporation Tax rate.

ERIS Rates

Alongside the merged scheme, ERIS offers additional support. It applies where:

- The company is loss-making and

- At least 30% of total expenditure relates to qualifying R&D

The Enhanced R&D Intensive Support (ERIS) provides a higher rate of relief for qualifying loss-making SMEs.

Businesses meeting the 30% R&D intensity threshold may secure a larger payable credit compared to the merged scheme.

Book a quick call back

PAYE/NIC Cap

Payable credits are capped using the formula: £20,000 + 300% of PAYE/NIC liabilities.

Free R&D Tax Credit Calculator

Find out how much you could claim with our R&D Tax Credit Calculator.

What are the Rules for Contracted-Out R&D?

Subcontracted R&D refers to research and development that your business has outsourced to a third party.

Under the R&D Merged Scheme, HMRC applies the “intended and contemplated” test to determine who can claim R&D tax relief. This means HMRC will assess which party to a contract:

- Originally intended or contemplated that R&D would be carried out,

- Bears the financial risk, and

- Retains decision-making authority over the work

In most cases, the commissioning company (the one directing and funding the R&D) will be the one eligible to claim. Subcontractors usually cannot claim, as they are performing work on behalf of another party.

Can I Claim Overseas Expenditure Under the R&D Merged Scheme?

Under the merged R&D scheme, payments for overseas R&D are subject to stricter rules:

- Externally provided worker (EPW) payments depend on where the work happens

Relief for EPWs generally only applies if the actual R&D activity occurs in the UK. However, if the work cannot be carried out in the UK, HMRC may make an exception.

- EPW costs usually require UK PAYE and NI

External workers’ wages that are paid via UK PAYE and include Class 1 National Insurance contributions will meet the criteria. If not, you may still qualify if you have a valid reason.

- Recognised “mandatory overseas” exceptions

There are narrow exceptions – if research and development must be done abroad (e.g. due to geographical, legal access, or environmental reasons), those costs may still qualify.

These exceptions are fully outlined under section 6.1 of HMRC’s draft guidance.

- Supporting documentation is essential

Even though you don’t submit detailed location records upfront, HMRC expects you to hold documentation to prove your eligibility.

This includes:

- Contracts specifying UK work

- Timesheets

- Evidence of PAYE/NI for EPWs

If audited, you’ll need to demonstrate where the R&D took place.

How Can I Apply for Tax Relief Under the Merged R&D Expenditure Scheme?

To claim for R&D tax relief, you’ll need to:

-

- Submit a Claim Notification Form (CNF) – if you’re new to R&D tax relief, or haven’t claimed in the last three years, you must submit a CNF within six months of your accounting period end

- Complete an Additional Information Form (AIF) – since August 2023, all claims must include an AIF, setting out your technical project details and financial breakdown (HMRC guidance)

- Submit your claim – ensure your CT600, company accounts, and AIF are aligned. Avoid common pitfalls such as missing the CNF or providing incomplete supporting evidence

HMRC recommends that you work with a specialist throughout the claims process to ensure you get the most out of your application.

Read our Guide to R&D Tax Relief in 2025 to learn if you qualify for ERIS.

Case Studies & Lessons Learned

Claiming errors can result in delays, failure to qualify or penalties.

R&D merged scheme example:

Case Study 1: Contracted-Out R&D Misclaim

A UK business outsourced part of its research project and incorrectly included subcontractor costs as eligible expenditure. HMRC rejected the claim due to strict rules on contracted-out R&D for SMEs.

Key lessons:

- Always check HMRC’s R&D guidelines before including subcontractor costs

- Keep clear records of qualifying activity and costs

- Seek professional advice to avoid misclaims

R&D Merged Scheme: A Complete Guide to Eligibility & Claims – FAQs

When Does My Company Switch to the Merged Scheme?

Most companies will move to the merged R&D scheme for accounting periods starting on or after 1 April 2024.

Can Subcontractors Still Claim?

Subcontractor rules vary between SMEs and large companies, so eligibility must be checked carefully.

Can I Claim for Overseas R&D?

From April 2024, overseas R&D costs are restricted unless meeting specific exemptions.

Does the PAYE/NIC Cap Apply to ERIS claims?

Yes, ERIS is subject to the PAYE/NIC cap.

What Happens If I Miss the CNF Deadline?

Missing the Claim Notification Form deadline generally means you cannot submit a claim.

Can I Claim if I Received a Grant?

Yes, but the type of grant may affect relief eligibility.

What if My Year-End Changes?

A change in year-end could impact which scheme applies.

How Can Alexander Clifford Help?

Completing your claim without the help of a specialist could hinder your chances of getting the full entitlement you deserve.

As leading R&D tax credit specialists, we simplify the R&D tax credits claim process, enabling innovative businesses to grow.

Maximise your entitlement and boost your revenue with a claim that ticks all of the right boxes.

Get a decision on your R&D eligibility from a qualified specialist in 15 minutes.