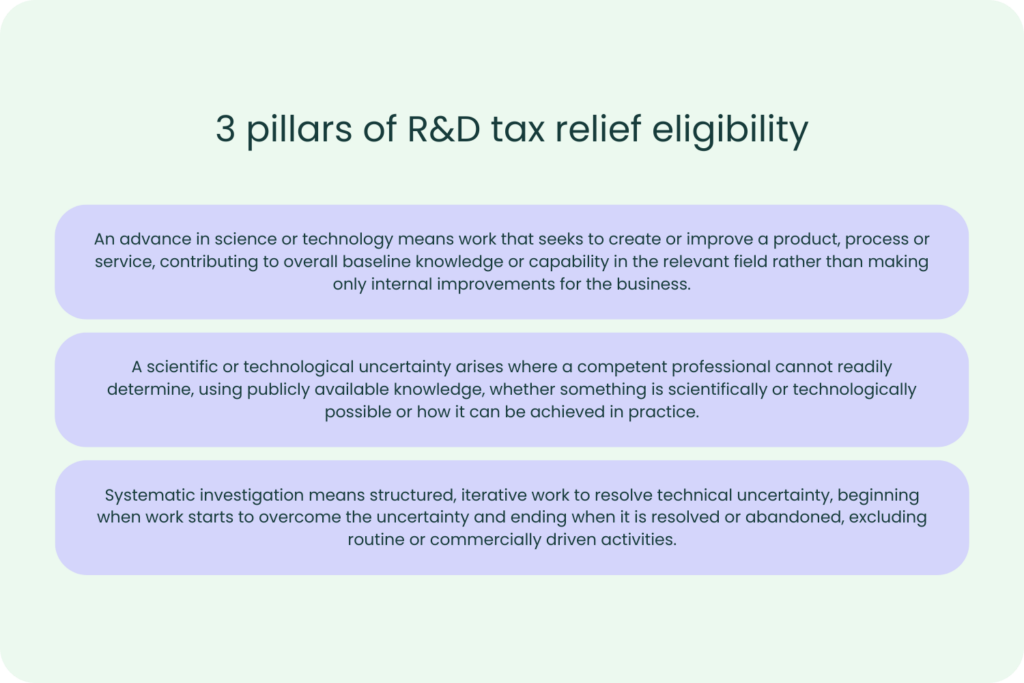

When it comes to claiming R&D tax relief, a project must be able to clearly demonstrate an advance within a field of science or technology. To qualify for R&D tax relief, the company must clearly define the baseline level of knowledge and the specific scientific or technological uncertainty that needs to be resolved.

There are many companies that are still unsure what counts as a scientific or technological uncertainty. In HMRC terms, this arises where a solution is not readily deducible by a competent professional working within the relevant field.

In this article, we are going to be discussing the topic of scientific and technological uncertainty. From the definition to how competent professionals need to assess activity to see if it qualifies for claiming R&D tax credits.

What is the definition of ‘scientific or technological uncertainty’?

A full definition of scientific or technological uncertainty can be found in the DSIT guidelines. In R&D tax relief claims, scientific or technological uncertainty exists where it is not clear how to achieve an outcome using existing knowledge or methods. Therefore, the project will need to demonstrate that the solution was not readily deducible by a competent professional who works within the relevant field.

Scientific or technological uncertainty in R&D tax credit claims drives the need for qualifying activity. Where uncertainty exists within a project, the company must be able to show how it was identified and how it was addressed through technical work.

What qualifies as a scientific or technological uncertainty?

There are some key indicators when it comes to defining genuine uncertainty, here are four key areas to look for:

Unexpected scientific or technical setbacks

These setbacks may indicate genuine uncertainty where challenges arise that could not have been resolved using existing knowledge.

This can include:

- Repeated failures during prototyping

- Unexpected behaviour in systems or materials

- Performance outcomes that differ from expected results

These setbacks must reflect gaps in scientific or technological understanding, rather than routine defects or correctable errors.

Fundamental unknowns

These will arise where there is insufficient knowledge about whether a particular outcome is achievable at all.

This may involve:

- Working with new materials

- Developing novel products

- Attempting to apply existing technologies in ways that have not previously been proven

The key point is not that the company lacks experience, but that a competent professional working in the field would not have a clear or accessible solution.

Solutions that were not readily deducible

This is a core feature of qualifying scientific or technological uncertainty. Even where the desired outcome is understood, the method for achieving it may not be readily deducible by a competent professional. If resolving the challenge requires experimentation, iteration or the process of developing new techniques, this supports the presence of genuine uncertainty. However, if the solution can be resolved through standard practice or existing guidance, it is unlikely to qualify for R&D tax credits.

Methodological unknowns

The uncertainty must relate to how a scientific or technological advancement can be achieved. This can occur where multiple approaches already exist, but certainty of success is unclear. In these cases, undertaking structured testing and analysis is required to identify a suitable method. This goes beyond routine optimisation and reflects an effort to overcome scientific or technological limitations. The uncertainty must extend beyond what is readily achievable using existing knowledge and require a systematic attempt to resolve through scientific or technological work.

What does not qualify as a scientific or technological uncertainty?

During a project, not every uncertainty that a company faces will meet the criteria of a qualifying scientific or technological uncertainty. Many projects involve difficulties, but this alone does not make them eligible for R&D tax relief. If a solution can be identified by either reviewing existing knowledge or through straightforward development, or just by applying the required time and resources, it is unlikely that it qualifies as genuine research and development.

A common issue is misidentifying the technical uncertainties. For an activity to qualify for R&D tax credits, the uncertainty must relate to whether the underlying science or technology can be achieved in practice, and not be readily deducible by a competent professional. Challenges such as resource shortages, project timelines or market demand do not meet the criteria.

On the other hand, attempting to achieve a scientific or technological outcome in a new or more efficient way, such as exceeding the performance or efficiency of existing methods, may represent a genuine scientific or technological uncertainty if it requires advancing knowledge or methods in the relevant field. Improvements that rely on existing methods or standard practice will not qualify.

HMRC R&D tax relief guidance states that activities which use readily available methods and do not involve technical uncertainty, along with cosmetic changes and standard system upgrades, fall outside the scope of qualifying R&D.

While challenges may arise during a project, a qualifying scientific or technological uncertainty must be central to the activity undertaken. A structured attempt to resolve the uncertainty, rather than routine problem-solving is required to qualify for R&D tax relief.

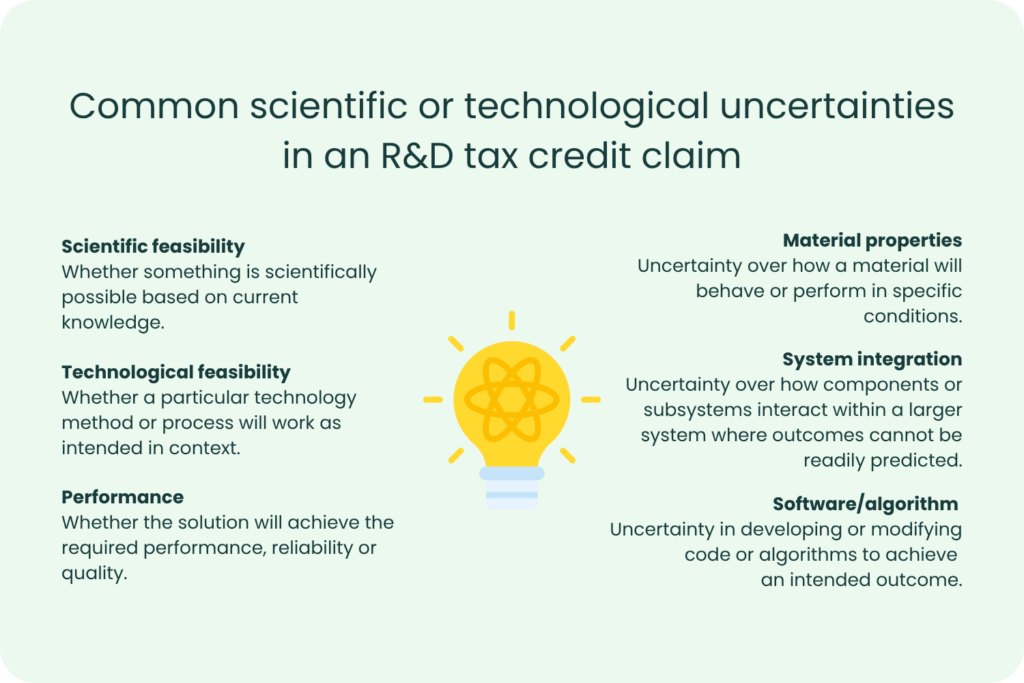

What are examples of scientific or technological uncertainties across different industries?

While the qualifying criteria for scientific or technological uncertainty remain consistent, how they arise in practice varies by industry. Below are some different examples of scientific or technological uncertainties for various industries:

Engineering and manufacturing– Uncertainty may relate to material behaviour, achieving required levels of precision or performance, or developing new production methods that have not yet been established and cannot be readily deduced using existing knowledge.

MedTech– Examples of uncertainty within the MedTech sector can involve material compatibility, integrating hardware and software systems, or achieving reliable performance where existing methods do not provide a clear solution.

Software development– Uncertainty may arise in achieving the required performance, processing large amounts of data, or integrating systems where compatibility is not fully understood.

In each case, the common factor is that the outcome cannot be readily achieved using existing knowledge or standard methodologies, and would not be readily deducible by a competent professional working in the field.

How are scientific or technological uncertainties evidenced?

Identifying scientific or technological uncertainties is only one part of the R&D tax relief claim process. Companies must also retain evidence including technical logs, reports, information regarding the technical unknowns, failed attempts and development work undertaken.

The evidence should accurately reflect the work undertaken throughout the project. This may include:

- Technical documentation

- Design iterations

- Test results and analysis

- Internal discussions or decision records

The key is that the evidence supports the technical narrative. It should demonstrate that the scientific or technological uncertainty was recognised and that a structured attempt to resolve it was addressed.

Why does clear identification of scientific or technological uncertainties matter?

Correctly identifying scientific or technological uncertainty is essential for submitting a robust R&D tax credits claim.

If uncertainty is overstated, there is a risk of non-compliance. If it is understated or missed entirely, companies may fail to claim eligible research and development activity. This may also increase the likelihood of an enquiry, which can delay the claim.

A well-defined uncertainty provides the foundation for the R&D tax credit claim. It shapes the technical narrative, supports the identification of qualifying activity and underpins the assessment of eligible expenditure.

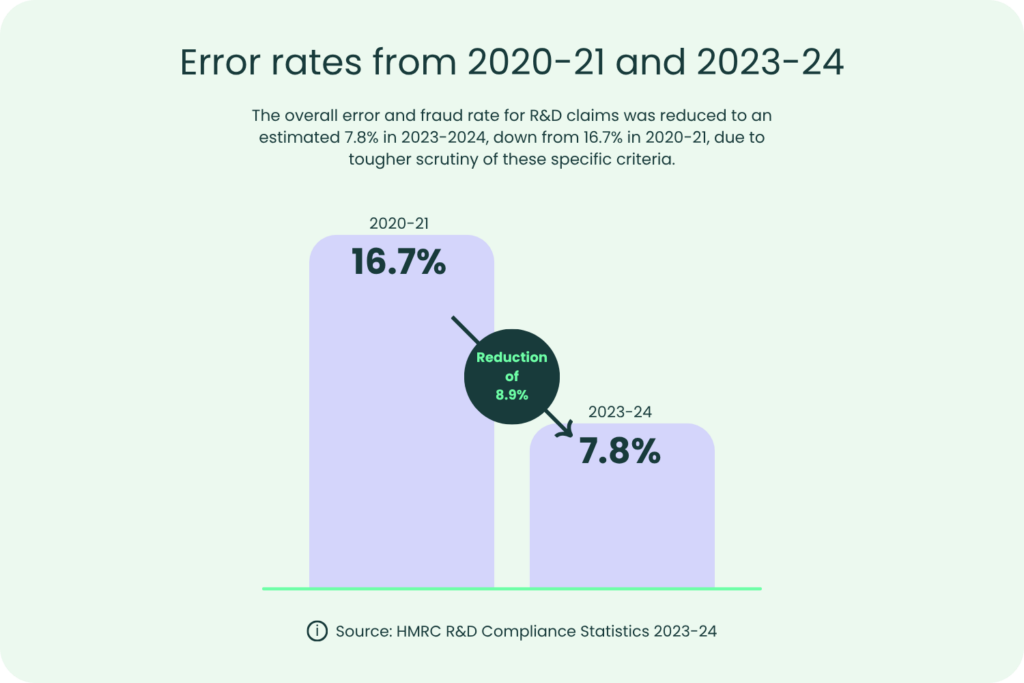

This is reflected in HMRC’s reported error and fraud rates, which highlight the level of scrutiny applied to these criteria.

How does uncertainty drive qualifying R&D activity?

Scientific or technological uncertainty is not just an aspect of eligibility. It is what drives the qualifying R&D activity itself.

Where scientific or technological uncertainty exists, companies undertake a structured programme of work to resolve it. This typically involves:

- Defining a technical objective

- Identifying the limitations in currently available methods or knowledge

- Testing potential solutions to the uncertainty

- Analysing results and refining the approach

Early attempts to resolve uncertainty may fail or produce inconclusive results. This does not disqualify the work undertaken. In many cases, it will reinforce the presence of genuine scientific or technological uncertainty.

What matters is that the activity is aimed at resolving uncertainty that would not be readily deducible by a competent professional, rather than applying existing knowledge or standard methodologies.

What does HMRC expect to see in an R&D claim?

HMRC expects clear and compliant documentation of the scientific or technological advancement sought, the scientific or technological uncertainties encountered and the R&D activity undertaken to resolve them. This should define what capability, performance or reliability did not previously exist.

It is also important to outline why the outcome was not readily deducible by a competent professional based on the available baseline knowledge. It should also include the existing knowledge and methods considered, and why these were insufficient during the process of resolution.

The technical narrative should describe the structured approach taken including:

- Hypotheses

- Testing

- Prototyping

- Analysis

- Technical decision-making

The technical narrative and any supporting documentation should accurately reflect the activity undertaken, including partial successes and any new knowledge generated through attempts to resolve the uncertainty. This should be supported by contemporaneous evidence such as experiment logs, technical documentation, design reviews, test data, or version-controlled artefacts, with qualifying costs aligned to the activities addressing those uncertainties.

Closing thoughts

A common area where R&D claims succeed or fail is in the identification of scientific or technological uncertainty. This requires more than a high-level description of a project. It depends on clearly demonstrating where existing knowledge was insufficient and how the uncertainty was addressed through a structured approach.

Many R&D tax relief claims fall short because the uncertainty is not clearly explained or properly supported. This can result in missed eligible expenditure or an HMRC enquiry.

At Alexander Clifford, we focus on identifying genuine scientific or technological uncertainties, establishing the baseline level of knowledge, and building clear, well-supported technical narratives that reflect the work undertaken.

Our approach is evidence-led and grounded in HMRC guidance. We ensure that each claim clearly aligns the uncertainties, the qualifying activity and the associated expenditure, so it is both accurate and defensible.

If you are looking to improve how scientific or technological uncertainty is identified and presented in your R&D tax relief claim, we can support you in taking a more structured and compliant approach. Please get in touch to speak with a member of the team.