When it comes to R&D projects, work such as software development, engineering design, laboratory testing or specialist consultancy work is often delivered by external providers.

The structure of the relationship between the claimant company and the external provider matters for R&D tax relief purposes. Subcontracted R&D expenditure can materially affect the value of a claim, particularly where connected group companies are involved in the project.

In this article, we are going to be discussing what connected and unconnected companies are and how they are important in a UK R&D tax relief claim.

What does HMRC mean by connected companies?

HMRC uses specific legislative definitions within the R&D tax relief regime. They do this to ensure compliance and consistency is followed throughout the documentation.

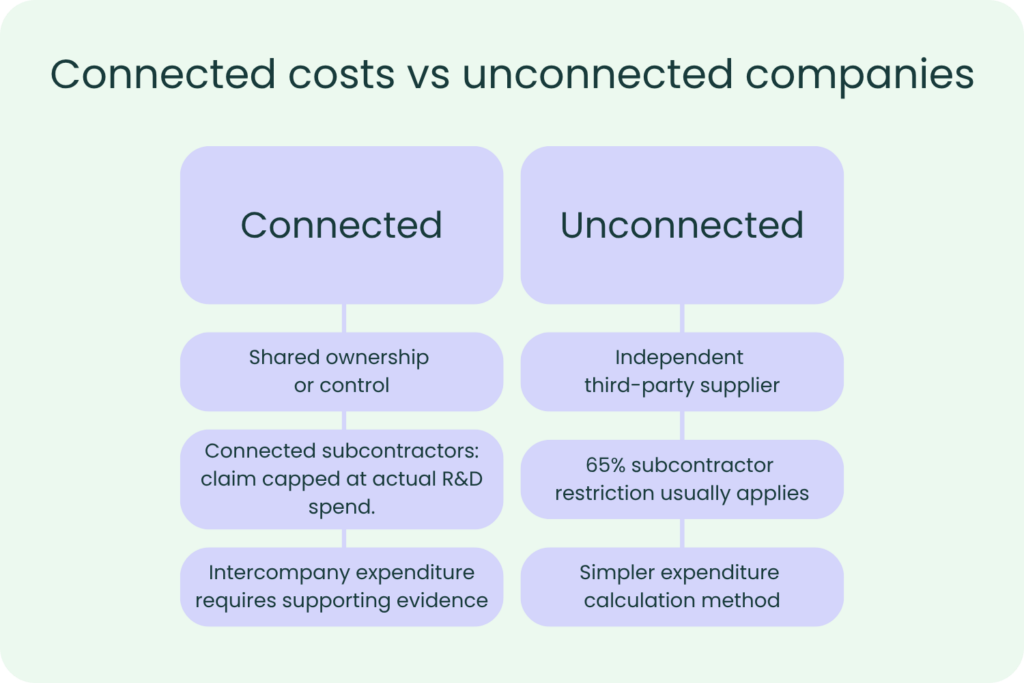

‘Connected companies’ is a term that refers to businesses where one company has direct or indirect control over another.

For example, if a company owns 100% of another company, this means that they are connected. If two companies are owned by the same holding company, they are also generally treated as connected for R&D tax purposes.

This distinction matters where subcontracted R&D expenditure is included within a claim, as connected and unconnected companies each have their own rules under the legislation.

What does HMRC mean by unconnected companies?

HMRC uses the term ‘unconnected companies’ to describe businesses that do not have direct or indirect control over one another. In simple terms, they are independent third-party companies with no shared ownership or control over business operations.

For example, if a company engages an external software developer, engineering consultancy, or testing laboratory that operates independently from the claimant business, HMRC would generally treat that supplier as an unconnected company.

This distinction is important because unconnected subcontractor costs are usually subject to the standard 65% restriction within an R&D tax relief claim. HMRC applies this rule to account for elements such as profit margin and non-qualifying overheads included within the subcontractor’s invoice.

Understanding whether a supplier is connected or unconnected helps ensure subcontracted R&D expenditure is treated correctly and calculated in line with HMRC’s legislation.

Why do connected company relationships matter in an R&D tax relief claim?

Connected company relationships can directly affect how qualifying R&D expenditure is calculated and evidenced within a claim. HMRC applies additional scrutiny where subcontracted R&D activity takes place between companies under common ownership or control.

This is particularly relevant within group structures where research and development activity is shared across multiple entities. In these arrangements, businesses must clearly demonstrate which company carried out the qualifying work, which entity incurred the expenditure, and how the costs relate to the underlying R&D activity.

For example, a parent company may coordinate an R&D project while a subsidiary company performs part of the technical development work. Where costs are transferred between connected entities, HMRC may expect businesses to provide supporting evidence showing how the expenditure was calculated and whether the costs directly relate to qualifying R&D activity.

Qualifying expenditure may include costs connected to the R&D work undertaken, such as:

- Staff salaries

- Employer NIC contributions

- Pension contributions

- Software directly used within the project

- Consumable items used during development or testing

Businesses should also maintain contemporaneous documentation supporting the relationship between the companies involved and the work carried out. This may include intercompany agreements, project records, technical documentation, invoices, and internal cost allocation records.

Incorrectly applying connected company rules or failing to evidence the relationship between entities can increase the likelihood of HMRC scrutiny and lead to amendments within the claim process.

What evidence should businesses retain for subcontracted R&D activity?

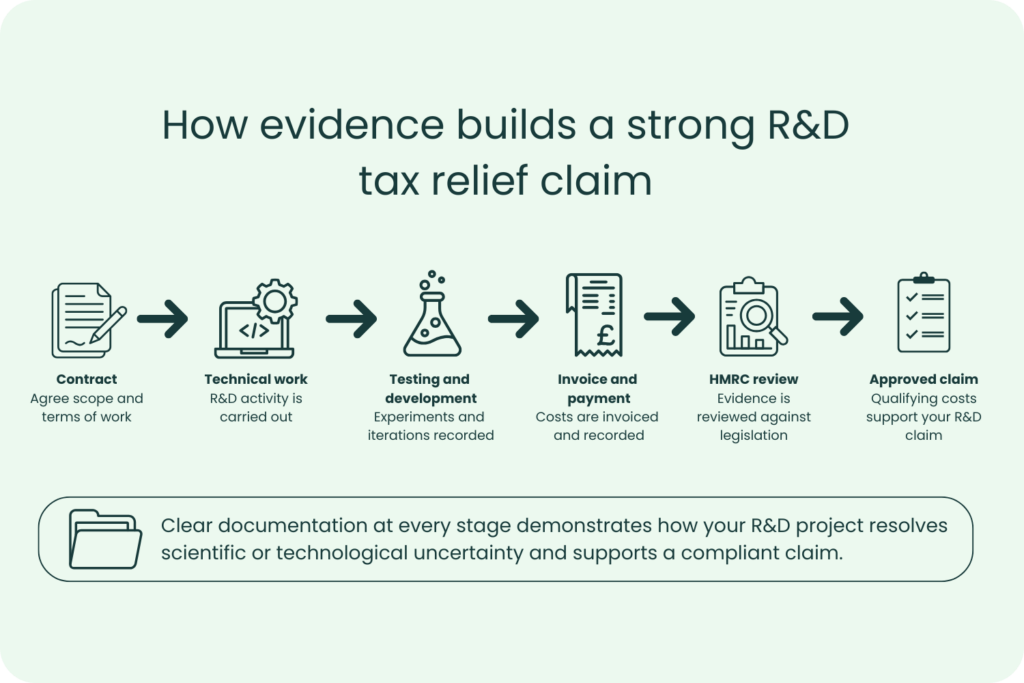

Where subcontracted R&D activity forms part of a claim, businesses should retain clear supporting evidence showing how the work contributed to the wider project and why the expenditure qualifies under HMRC’s R&D legislation.

The subcontracted activity must still relate directly to resolving scientific or technological uncertainty within the project. HMRC may expect businesses to explain how external contractors, consultants, or connected companies contributed to the qualifying R&D activity undertaken.

Qualifying subcontracted R&D work commonly includes:

- Software development work

- Engineering design and testing

- Prototype development

- Specialist scientific analysis

- Technical feasibility studies

Supporting evidence should normally include:

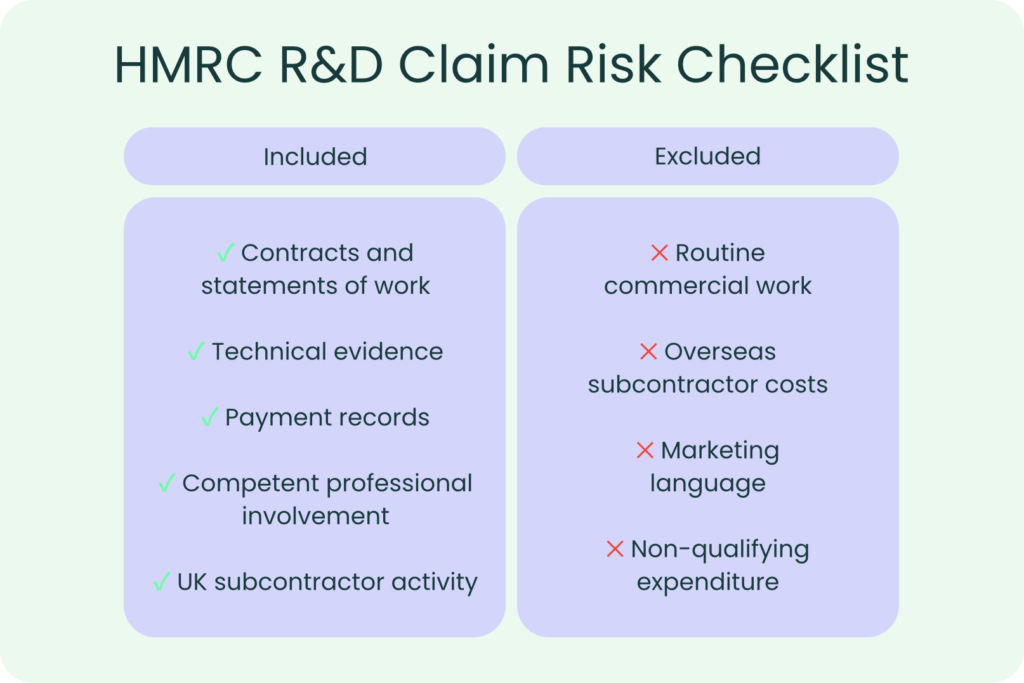

- Contracts or statements of work

- Invoices and payment records

- Technical specifications

- Project timelines

- Internal project communications

- Evidence prepared by competent professionals involved in the work

Maintaining clear records is particularly important where multiple companies or third-party suppliers contribute to the same R&D project. HMRC often reviews whether the technical narrative, accounting records, and subcontracted expenditure align consistently throughout the claim.

Businesses should also ensure that non-qualifying commercial activity, routine development work, and general operational costs are excluded from the calculation. Accurate record keeping can help reduce compliance risks and support a stronger position in the event of HMRC enquiries.

What are some common mistakes that companies make during the R&D claim process?

Without specialist support from a reputable R&D tax credit advisory, companies can make mistakes during the R&D claim process which then becomes a compliance risk.

Some common mistakes include:

1. Missing the Additional Information Form (AIF)

The Additional Information Form is one of the core documents that supports an R&D tax credit claim. If a company does not submit an AIF, HMRC will automatically reject the claim.

2. Missing deadlines

R&D claim deadlines are strict and must follow the guidelines set out by HMRC. If a company submits a claim outside the permitted timeframe, the claim will be rejected.

3. Not submitting a Claim Notification Form (CNF) within the timeframe of the company’s year end

The Claim Notification Form is another core part of the claim process. HMRC must be notified that the company intends to claim R&D tax relief. This notification must be submitted within six months of the end of the accounting period. Since its introduction, this requirement has created difficulties for some businesses unfamiliar with the process.

4. Mistakes in the technical narrative

From routine commercial work to using vague marketing language, these mistakes can increase the risk of HMRC scrutiny. R&D is only about seeking an advance in science or technology; it does not cover routine business development.

Businesses should also avoid unsupported phrases such as “cutting-edge” or “revolutionary” without explaining the underlying scientific or technological uncertainty involved and why existing publicly available knowledge could not easily resolve the issue.

5. Including non-qualifying expenditure

Routine business costs, general travel expenditure and patent-related costs are not qualifying expenditure for R&D tax relief purposes.

6. Applying under the incorrect scheme

If a company submits a claim under the incorrect R&D scheme, the claim will require amendments or further HMRC review. Businesses should ensure they understand which scheme applies to the accounting period and company circumstances before submission. If your business has been affected by this, we can help!

7. Misunderstanding subcontractor rules

Under the new merged scheme, there were some changes made to the claiming process. This meant that overseas subcontractor costs are now disallowed to focus more on the innovative side of a project. The claim for subcontractor costs, the work must be carried out in the UK, exceptions may apply.

How can the risks of an HMRC enquiry be reduced?

In recent years, HMRC has increased their level of scrutiny with the claiming process. This increased level of scrutiny is particularly regarding where subcontracted expenditure and group company arrangements are involved. An enquiry does not mean that the R&D claim is incorrect. HMRC expects businesses to maintain clear supporting evidence and apply the legislation accurately as this will put the business in a stronger compliance position.

One of the most important steps is correctly identifying whether subcontractors are connected or unconnected businesses before calculating any qualifying R&D expenditure. Applying the incorrect treatment can result in overstated costs within the claim which raises risks of incompliance.

Businesses should also maintain detailed contemporaneous documentation that aligns with the R&D activity undertaken. This may include:

- Contracts and statements of work

- Project timelines and technical specifications

- Records of invoices and payments

- Internal project conversations

- Technical reports or testing documentation

- Evidence prepared by competent professionals involved in the work

Where subcontracted R&D activity is included, companies should clearly outline how the work contributed to resolving scientific or technological uncertainty within the wider project. HMRC often expects the technical narrative and financial documentation to align with one another.

For connected company arrangements, maintaining detailed cost breakdowns is particularly important. HMRC may request evidence showing how the qualifying expenditure was calculated and whether intercompany charges reflect the actual R&D costs incurred during the project.

Businesses should also ensure that:

- The claim methodology is applied consistently

- Project descriptions accurately reflect the work undertaken

- Non-qualifying commercial or routine activity is excluded

- Costs can be verified against accounting records where necessary

Do you want to know whether your project qualifies for R&D tax relief?

At Alexander Clifford, we focus on ensuring that all technical and financial documentation is supported by genuine R&D activity evidence and calculated in line with HMRC’s legislation. From the initial phone call consultation to the final payout, we support you step-by-step in this submission to give your business the best chance of claiming R&D tax credits.

If you would like further guidance on connected and unconnected subcontractor costs, our team of financial and technical specialists will guide you through the answers with a clear and compliant approach. Please contact us for more information.