The term “not readily deducible” refers to a situation where a competent professional could not resolve a scientific or technological uncertainty, or achieve an advance, using existing knowledge, publicly available information, or standard industry methods. Activity of this kind is not considered routine and may qualify as R&D.

In this article, we explain what HMRC means by “not readily deducible” in R&D projects. We outline how this is assessed, how it links to scientific or technological uncertainty and what it means for identifying qualifying research and development activity.

What is the definition of “not readily deducible”?

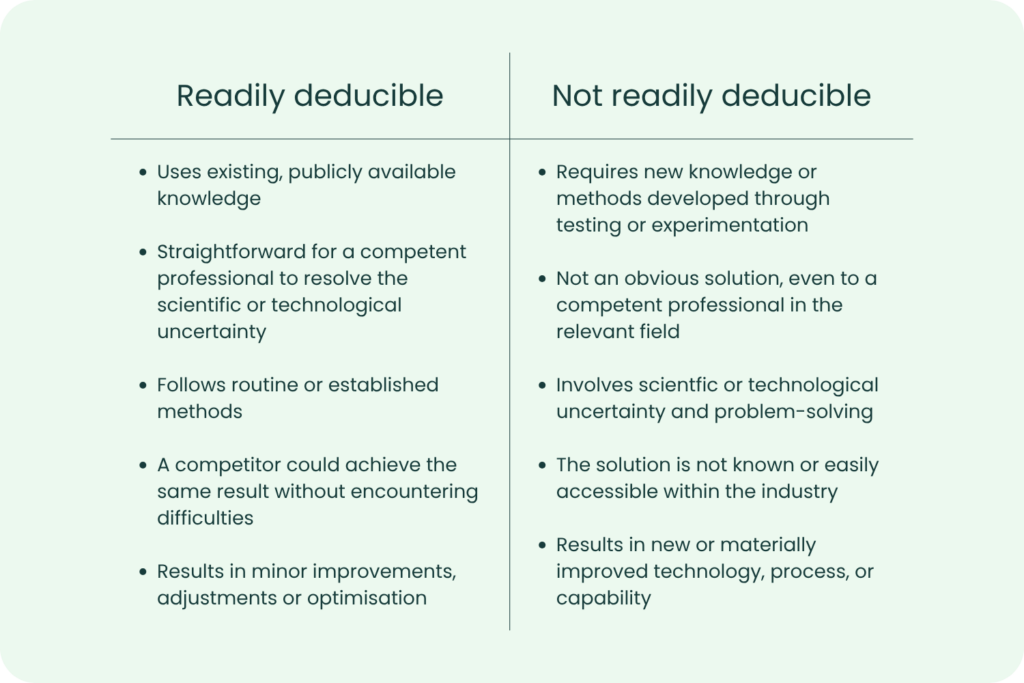

“Not readily deducible” describes work that goes beyond standard practice. If a competent professional could resolve the scientific or technological uncertainty using existing knowledge or established methods, the solution would be considered readily deducible and would not qualify for R&D tax relief.

For activity to qualify as R&D, it must involve resolving uncertainty that cannot be addressed through applying routine methods or available knowledge. This often requires structured evidence such as experimentation or analysis. If the outcome is not easily achievable by a competent professional, this indicates genuine scientific or technological uncertainty.

How does HMRC assess whether something is not readily deducible?

HMRC does not treat “not readily deducible” as a standalone test for qualifying R&D activity. It forms part of the wider assessment of whether a project seeks to resolve a scientific or technological uncertainty.

As part of this assessment, HMRC considers whether a competent professional could identify a solution using available baseline knowledge and established methodologies, without the need for further investigation or experimentation.

In practice, this assessment focuses on three areas: baseline knowledge, the level of uncertainty and the process undertaken to resolve it.

Baseline knowledge

HMRC evaluates what was already known or publicly available at the time the activity was carried out. This includes published material, standard methodologies and common industry practices.

If the solution could be derived from this baseline knowledge using established methods, the activity is unlikely to align with HMRC’s qualifying criteria.

In practice, defining baseline knowledge requires more than a general statement of what was known. Baseline knowledge should reflect what a competent professional in the relevant field could be expected to reasonably understand at the outset of the project. This may include:

- Technical documentation

- Standard tools or frameworks

- Comparable systems already in use

It is not necessary for the business to have direct knowledge of all available information. The assessment is based on whether that knowledge was accessible and could have been used by a competent professional to resolve the scientific or technological uncertainty. Setting this baseline clearly explains why the outcome could not be derived from existing knowledge.

The level of uncertainty

The key question is whether there was genuine scientific or technological uncertainty. The uncertainty must not be resolvable through routine analysis or applying existing knowledge or methodologies.

This includes situations where it is unclear whether a scientific or technological solution is achievable entirely, or how it can be achieved in practice.

The process undertaken

HMRC also considers the work carried out to reach the solution. This includes activities such as testing, iteration, simulation and prototyping. These activities indicate that the outcome was not known at the outset. They show that the work involved resolving scientific or technological uncertainty rather than applying a predefined solution.

However, the presence of these activities alone is not sufficient. They must be directed at resolving a genuine scientific or technological uncertainty. Repeating known approaches or applying standard methods in different combinations does not in itself demonstrate that the outcome was not readily deducible.

This approach reflects the principle that qualifying R&D activity is defined by the presence of uncertainty, not the success or commercial value of the outcome.

How should “not readily deducible” be evidenced?

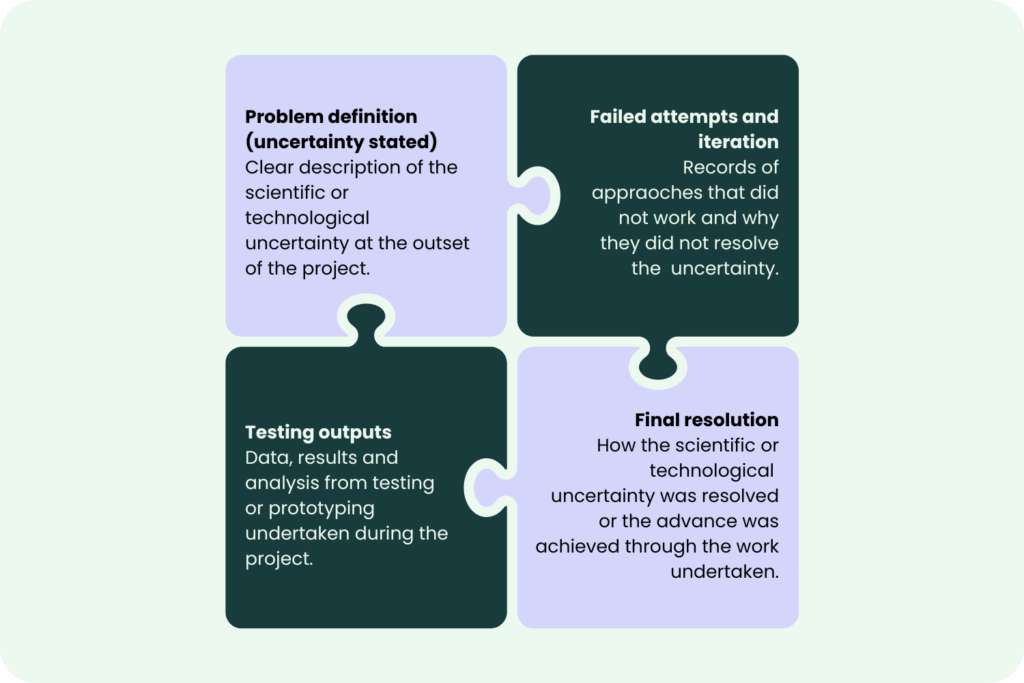

HMRC’s assessment is based on what can be demonstrated, not just what is described. Supporting evidence is therefore important in showing that the outcome was not readily deducible.

This evidence may include technical documentation, records of testing and iteration, performance data and any internal discussions between competent professionals who are working on the project. Relevant evidence demonstrates how the scientific or technological uncertainty was approached and why existing knowledge or methods were not sufficient to resolve it.

The focus should be on contemporaneous and technically relevant evidence that shows how the uncertainty was approached.

In many cases, explaining why standard approaches were considered and did not resolve the issue provides stronger support than describing the final solution alone. Claims often fall short not because the uncertainty did not exist, but because it was not clearly evidenced within the documentation. Without this context, HMRC may conclude that the work followed established methods.

How does HMRC define a competent professional?

A competent professional is defined as an individual with the relevant knowledge and experience in the field of the project taking place. This may be a single individual or a team working to resolve the uncertainty.

The assessment considers whether the team or person could readily resolve the scientific or technological uncertainty using existing knowledge or methods. If they could not, the work may meet the criteria for R&D tax relief.

It is also important to note that the term “not readily deducible” does not mean that something was costly, complex or difficult. A project may involve significant effort and still rely on available knowledge or established methods. In these cases, the outcome remains readily deducible.

What are some examples of a project being ”not readily deducible”?

The following examples demonstrate how HMRC distinguishes between qualifying and non-qualifying research and development activity:

Qualifying (not readily deducible)

A company attempts to combine standard components to meet a specific space constraint, but the solution cannot be achieved using established methods. The team then carries out simulation and develops prototypes to determine whether the required performance can be achieved. The outcome cannot be established at the outset using available knowledge.

Non-qualifying (readily deducible)

A software developer uses existing libraries to build a website with a new layout. Although the outcome is new to the business, the methods required are well understood and publicly available. The solution can be achieved using established techniques and is therefore readily deducible.

How does “not readily deducible” link to technical uncertainty?

The term “not readily deducible” lies within the definition of scientific or technological uncertainty set by HMRC.

A project could involve research and development activity where a competent professional cannot readily resolve whether something is scientifically or technologically possible, or how it can be achieved through using existing knowledge.

The test is not based on time, cost, or the involvement of skilled professionals. It is based on whether the uncertainty goes beyond routine problem-solving and requires an advance in the field.

Where a solution is already available, or could be derived from existing knowledge using established methods, the activity is unlikely to meet the criteria for R&D tax relief.

What are some common misconceptions about “not readily deducible”?

There are several common misconceptions in this area.

- Cost does not determine eligibility

A project may involve significant expenditure and still be readily deducible if it relies on established knowledge.

- Difficulty is not the same as uncertainty

Work can be complex or time-consuming but still follow known approaches.

- Being new to the company is not sufficient

An activity may be new to the business but is well understood within the wider field.

- Trial and error alone is not sufficient evidence

Iteration must be directed at resolving a genuine uncertainty, not repeating known approaches.

How does HMRC approach this area in practice?

A common area where R&D claims succeed or fail is in demonstrating that the outcome was not readily deducible to a competent professional.

This requires more than just an in-depth description of the project. It depends on clearly explaining why the solution could not be determined using existing knowledge and how the work addressed that gap through a structured approach.

HMRC often focuses on what was known at the outset of the project and whether existing methods could reasonably have been applied. Where this is not clearly set out, there is a risk that the activity is viewed as routine.

A further consideration is how the area of uncertainty is outlined within the project. Sometimes, the uncertainty is not if a challenge exists, but whether it represents limited knowledge or methods in the current scientific or technological field. Where a project involves adapting existing solutions to meet commercial requirements, the outcome may still be readily deducible, even if the implementation is complex.

Where the work involves determining whether a solution is readily deducible, or identifying a method not described in existing knowledge, this indicates a scientific or technological uncertainty.

This requires a clear explanation of what was known at the outset and why that knowledge was insufficient.

Closing thoughts

In practice, R&D tax credit claims that clearly define this boundary between readily deducible and not readily deducible activity are more likely to align with HMRC’s criteria.

Qualifying R&D claims outline that not only that R&D activity was undertaken, but that it was in the attempt to resolve scientific or technological uncertainty rather than applying available methods or knowledge.

At Alexander Clifford, we focus on identifying where activity goes beyond established knowledge, defining the baseline level of understanding and building technical narratives that:

- Are clear and well-supported

- Can reflect why the outcome was “not readily deducible”

Our evidence-led and cautious approach has allowed us to ensure that each R&D tax relief claim clearly aligns with the scientific or technological uncertainties, the qualifying R&D activity and the associated expenditure. This makes the claim both defensible and accurate.

If you are seeking to improve how “not readily deducible” activity is identified and presented in an R&D tax relief claim, we can support your business in taking a more structured and compliant approach. Please get in touch to speak with a member of the team.