The role of a competent professional in an R&D claim is to provide a technical assessment based on relevant scientific or technological expertise. Their input helps establish whether the project required research and development to overcome scientific or technological challenges. This involves identifying whether the project sought an advance in science or technology and assessing whether genuine technical uncertainty was present.

Without clear technical input, it becomes difficult to demonstrate that a project sought an advance in science or technology or involved genuine technical uncertainty. This is often where weaker claims begin to fail under scrutiny.

In this article, we explain what defines a competent professional, the role they perform within an R&D claim and why their judgement is central to a compliant and well-supported submission.

What is the definition of a competent professional?

A competent professional is an individual with scientific or technological expertise who can assess whether work seeks a genuine advance and involves relevant uncertainty that cannot be readily resolved using existing knowledge.

In many cases, the competent professional is an in-house specialist with direct involvement in the project. They often have detailed knowledge of:

- The relevant industry context

- The project’s objectives & technical details

- The uncertainties encountered during development

How is a competent professional identified?

Before preparing an R&D claim, a company should identify the competent professional for each relevant project. For example, in a software project, this could be a lead developer or engineer. What matters is that the individual has relevant experience within the same scientific or technological field as the work being assessed.

For some companies, they may only have one person responsible for the project, in these cases, they would be the relevant person for the role of the competent professional.

However, other companies may have had several people working on the projects, this means they would have more than one competent professional assessing the project for qualifying R&D activities under the DSIT guidelines.

To support the process of claiming, it is beneficial to keep records of the project’s activities as they occur. This creates a clear audit trail, making it easier to evidence qualifying R&D activity, track technical uncertainty and support the judgement of the competent professional when preparing the claim.

What does a competent professional need to assess?

At an early stage, the competent professional assesses R&D activity taking into consideration four key areas.

These four areas are:

- What was the baseline knowledge?

- What was the advance being sought?

- What technical uncertainties were encountered?

- Where did the R&D activity begin and end?

From this assessment, the claim should be able to clearly outline the following:

- The baseline level of knowledge that was already established or could be reasonably deduced by a competent professional

- Why a clear or existing solution was not available at the start of the project or why existing solutions did not resolve the uncertainty encountered.

- The specific activities that directly contributed to resolving the scientific or technological uncertainty

How does HMRC decide who is a competent professional?

HMRC expects the project’s competent professional, or professionals, to clearly demonstrate relevant knowledge and experience within the scientific or technological field being assessed.

This supports the credibility of HMRC’s decision when assessing if the activities stated meet the definition of qualifying research and development activity.

Examples of this may include:

- Substantial experience working at an appropriate level within the field

- Relevant academic qualifications, supported by ongoing professional development

- A record of scientific or technical publications

- Other forms of professional or industry acknowledgement within the relevant field

Why is the role of a competent professional important?

The competent professional defines the technical position of the R&D claim process. An R&D tax relief claim requires someone who can explain the work undertaken in detail and support that explanation with relevant technical knowledge.

They must be able to demonstrate why the technical uncertainty was genuine, why it could not be resolved using readily available baseline knowledge and how the work sought an advance in the overall field of science or technology rather than representing routine development.

This is often where weaker R&D tax relief claims stand out. A project may appear complex but fail to clearly articulate the underlying scientific or technological uncertainty in a structured and compliant way.

Without a well-supported assessment from a competent professional, the work risks being interpreted as standard commercial activity rather than qualifying R&D activity, which can affect the validity of the claim and any resulting tax relief.

Does a competent professional need to prepare the R&D tax relief claim?

While a competent professional is not required to draft the R&D claim, they should guide the technical position from the outset and review it in detail ahead of submission.

External advisers are best placed to manage the submission process, document qualifying expenditure and prepare the final claim. The technical position and supporting documentation should be defined and presented by the competent professional.

The competent professional should support the definition of the:

- Underlying problem being addressed

- Nature of the technical uncertainty at the outset

- Activities that directly contributed to resolving that uncertainty

- Point at which work transitioned from qualifying R&D activity to routine or commercial activity

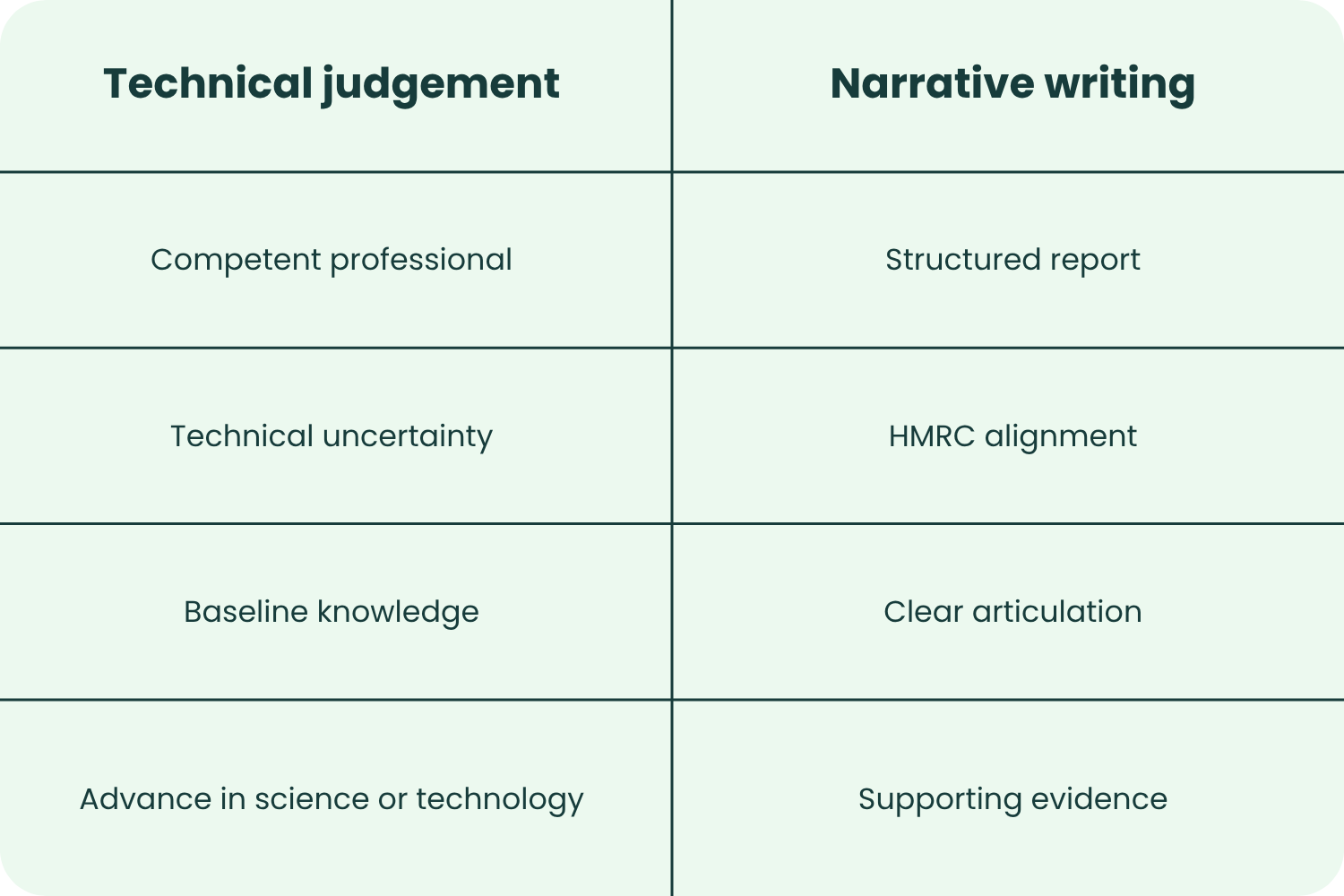

What is the difference between technical judgement and narrative writing?

There is a clear distinction between technical judgement and narrative writing within an R&D tax relief claim. Both are required as part of the claiming process, but they serve different purposes.

Technical judgement must come from the competent professional. It is based on their knowledge and experience within the relevant field. The competent professional will assess whether the work sought a genuine scientific or technological advancement, whether genuine uncertainties were present, and if these uncertainties were readily solvable with available knowledge at the time.

These uncertainties are addressed through the work undertaken during the project, not through existing baseline knowledge alone. This is a key area in determining if the activity qualifies as R&D.

Narrative writing is the process of documenting this technical position in a structured and compliant format. This is often carried out by external advisers who can prepare the narrative in a structure recognised and accepted by HMRC. This will be based on input from the competent professional.

A well-written report cannot compensate for weak or unsupported technical judgement. This also applies to technical work, the R&D claim can be undermined if it is not clearly presented.

In practice, the competent professional defines:

- The baseline knowledge within the field

- The nature of the scientific or technological uncertainty

- The work undertaken to resolve the scientific or technological uncertainty

- The point where the activity moves from R&D into routine development

When a narrative is prepared without sufficient technical input, it often leads to generic descriptions, unclear uncertainties or claims that rely on the commercial challenges rather than the scientific or technological ones.

When should the competent professional get involved in the R&D claim?

The competent professional should be involved throughout the lifecycle of a research and development project. Their role should not be limited to the preparation of the claim. Early and consistent input helps ensure that qualifying R&D activity is correctly identified and supported with appropriate evidence.

Typical activities for a competent professional would include the following:

- Beginning of the project

At the outset of the work, the competent professional should establish whether the work will involve significant scientific or technological uncertainties. Attempts to resolve this uncertainty will be the relevant advancement that the company is seeking to achieve. Reviewing the available methods and approaches to potentially solve the uncertainties will then establish the baseline and determine whether the activities undertaken qualify for R&D tax relief.

- Development phase

During the development phase, the involvement of the competent professional should continue as the work progresses to maintain continuity. Activities include reviewing how uncertainties are being addressed, ensuring that the activities remain within the scope of R&D, and supporting the documentation of key decisions, iterations and the outcome.

- Evolution of the project

As the project evolves, work will often move from resolving any uncertainty into routine or commercial activity. The competent professional should identify when this transition occurs, as it directly affects which activities can be treated as qualifying R&D activity.

- Reviewing the technical position

Before preparing the claim, the competent professional should review the technical position in detail. This requires them to include confirmation of the baseline knowledge, scientific or technological uncertainties encountered and activities that meet the definition of qualifying R&D.

In practice, late involvement from a competent professional could lead to gaps in evidence or unclear technical information which can weaken the credibility of the claim under HMRC guidance. Early engagement allows the R&D claim to be built on a foundation of consistency and support.

Closing Thoughts

Preparing and submitting an R&D tax relief claim requires a careful and structured approach. Each stage of the process should be handled with accuracy and clear supporting evidence. This reduces the likelihood of HMRC raising questions and helps ensure the claim reflects the underlying qualifying R&D activity.

If you are new to R&D tax relief, or your previous claims need a more robust approach, Alexander Clifford provides clear and compliant support throughout the process.

At Alexander Clifford, we work with businesses across a range of sectors to identify eligible projects, assess technical uncertainty and document qualifying activity in line with HMRC guidance. We focus on building well-supported claims that accurately reflect eligible expenditure and the work carried out by competent professionals.

Our strong track record is reflected in consistent client feedback and repeat engagements. Our approach is straightforward. We guide clients through this process of claiming and manage the technical narrative to ensure submissions are clear, accurate, and aligned with current HMRC expectations.

If you would like to understand how R&D tax relief may apply to your business, or you want to improve the quality of your existing R&D claims, get in touch.