For accounting periods beginning on or after 1 April 2024, the government replaced the SME and RDEC schemes with two new reliefs: the merged R&D scheme and Enhanced R&D Intensive Support (ERIS). The reforms were designed to create a more streamlined system while improving the integrity of R&D tax relief claims.

This article explains how the ERIS scheme operates, the eligibility criteria businesses must meet, how claims are submitted, and the common pitfalls that can impact a claim.

What is the ERIS scheme?

The Enhanced R&D Intensive Support (ERIS) scheme is a UK R&D tax relief incentive designed for loss-making SMEs that invest a substantial proportion of their expenditure in research and development. ERIS allows eligible companies to surrender trading losses in exchange for a payable tax credit which helps improve the business’ cash flow while continuing to invest in innovation.

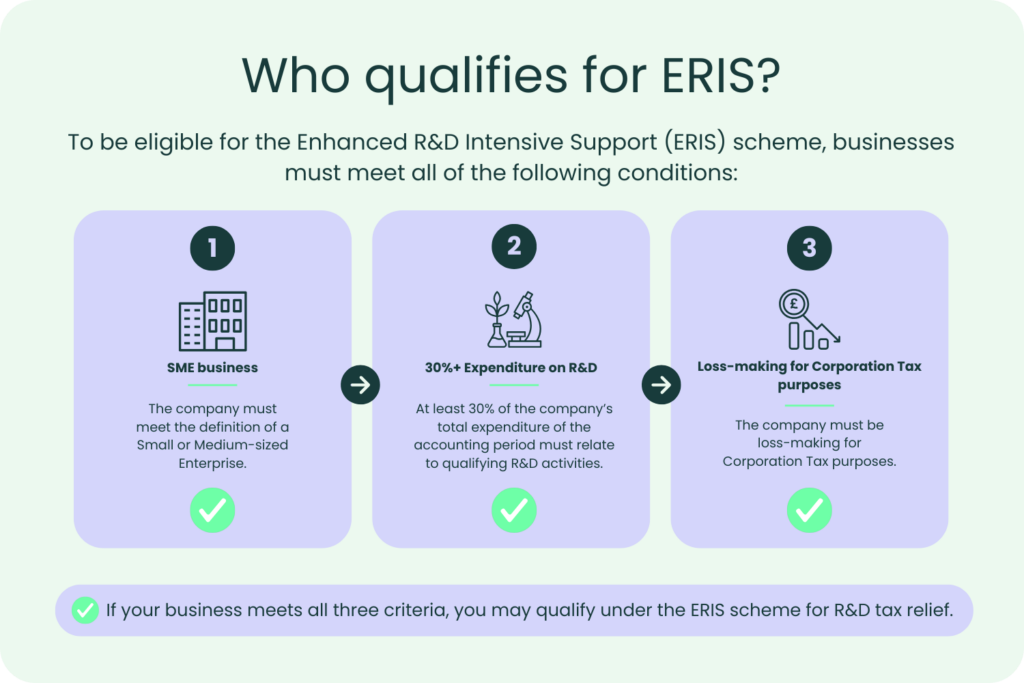

There are some specific conditions that businesses have to meet in order to qualify for R&D tax relief under the ERIS scheme:

- The company must meet the definition of a Small or Medium-sized Enterprise.

- The company’s qualifying R&D expenditure must represent at least 30% of its relevant total expenditure for the accounting period.

Loss-making position: The company must be loss-making for Corporation Tax purposes. Eligible businesses can surrender some or all of their trading losses in return for a payable tax credit under the ERIS scheme.

Businesses must be aware that only expenditure which meets the legislative criteria for qualifying R&D can be included in the R&D intensity ratio calculation. Companies should be able to clearly demonstrate that their projects sought an advance in science or technology and involved overcoming scientific or technological uncertainties.

How does the ERIS scheme work?

The Enhanced R&D Intensive Support (ERIS) scheme increases the level of tax relief available to loss-making SMEs that carry out qualifying research and development. It is intended to provide additional support to businesses where R&D forms a substantial part of their overall expenditure.

Under the ERIS scheme, qualifying companies can claim an enhanced deduction for eligible R&D costs. This increases the company’s trading loss for Corporation Tax purposes, which can then be surrendered in exchange for a payable tax credit from HMRC.

The process works as follows:

- Qualifying R&D expenditure is identified and included within the company’s Corporation Tax return.

- An enhanced deduction of 86% is applied to those qualifying costs, in addition to the normal 100% deduction already received through the accounts and tax computation.

- The resulting trading loss can be surrendered to HMRC in return for a payable tax credit.

- The payable credit is calculated at 14.5% of the surrendered loss, providing eligible businesses with a cash payment.

The ERIS scheme can provide eligible SMEs with a cash benefit of up to 27% of their qualifying R&D expenditure. For some loss-making companies, the payable credit can provide additional cash flow to support ongoing research and development activities.

As with any R&D tax relief claim, companies must be able to demonstrate that their projects sought an advance in science or technology and involved overcoming scientific or technological uncertainties. Only qualifying expenditure can be included in the calculation.

What is the merged scheme and how does it work?

The merged scheme refers to the UK’s primary Research and Development (R&D) tax relief incentive. It consolidates the previous SME scheme and the large company RDEC scheme into a single, streamlined system for accounting periods beginning on or after 1 April 2024.

Above-the-Line Credit: The core benefit operates as a taxable expenditure credit equal to 20% of qualifying R&D expenditure. After Corporation Tax, this delivers a net benefit of up to 16.2% of qualifying expenditure.

Simplified Subcontracting: Relief generally follows the company that decides to undertake and commission the R&D. The merged scheme also removes the previous SME restrictions relating to subsidised expenditure and many grant-funded projects.

Overseas Restrictions: Expenditure on subcontracted R&D and externally provided workers is generally only eligible where the work is carried out in the UK. Limited exceptions may apply where the conditions necessary for the R&D are not present in the UK and cannot reasonably be replicated here.

What are the differences between the two?

The main difference between the ERIS and the merged scheme is the level of support available and what type of company can benefit from each R&D tax relief scheme.

ERIS is specifically aimed at loss-making, R&D-intensive SMEs. It offers a higher potential cash benefit than the merged scheme, reflecting the government’s intention to provide additional support to businesses that devote a large proportion of their expenditure to research and development activities.

The merged scheme, by contrast, applies a single set of rules to most companies and is available regardless of whether a business is profitable or loss-making. This makes it the default route for many claimants who do not meet the ERIS eligibility requirements.

Key differences between these two R&D tax relief schemes include:

Eligibility: ERIS is only available to loss-making SMEs that meet the R&D intensity threshold. The merged scheme is available more broadly and is not restricted to R&D-intensive businesses making it universally accessible to businesses across the UK.

Level of relief: ERIS can deliver a higher effective cash benefit on qualifying R&D expenditure than the merged scheme, provided the company satisfies all eligibility criteria.

Loss surrender requirement: To access the enhanced support available under ERIS, a company must have sufficient trading losses available to surrender in exchange for a payable tax credit. Businesses without sufficient losses may find the merged scheme more suitable.

Claim flexibility: Where a company meets the ERIS eligibility conditions, the claim should be calculated under the relevant legislative conditions. The value of relief available will depend on the company’s qualifying expenditure, surrenderable losses and overall tax position.

The most appropriate scheme will depend on the company’s circumstances. Factors such as profitability, qualifying expenditure levels and available losses can all influence the value of a claim and the relief ultimately received.

Who can claim under the ERIS scheme?

The ERIS scheme is strictly reserved for companies that are loss-making for tax purposes. If a company is profit-making for Corporation Tax purposes, it cannot access this specific support and must instead claim R&D tax relief through the merged scheme.

How do SMEs claim under the ERIS scheme?

SMEs can claim under the Enhanced R&D Intensive Support scheme by demonstrating that they are loss-making, meet the 30% R&D intensity threshold and submit an Additional Information Form before filing their CT600.

Firstly, we recommend that the business checks the eligibility criteria before following through with an R&D claim. We advise this to avoid compliance errors and a possible enquiry being opened by HMRC later down the line. There are two schemes, the ERIS scheme and the merged scheme.

Next, we suggest that the business prepares strong and defensible technical and financial data. This evidence forms the foundation of the claim. It helps demonstrate that the project meets the legislative definition of qualifying R&D.

When filing an R&D tax relief claim under the ERIS scheme, there are some crucial submission steps to follow. The Additional Information Form (AIF) must be completed and submitted before the CT600 has been submitted. Without following this step, the claim will automatically be rejected.

What are some common mistakes encountered during the ERIS scheme process?

The Enhanced R&D Intensive Support (ERIS) scheme offers enhanced relief for loss-making SMEs, but the rules are strict. Most errors encountered during this process typically fall into three areas which are eligibility, cost calculations and compliance.

Eligibility Errors

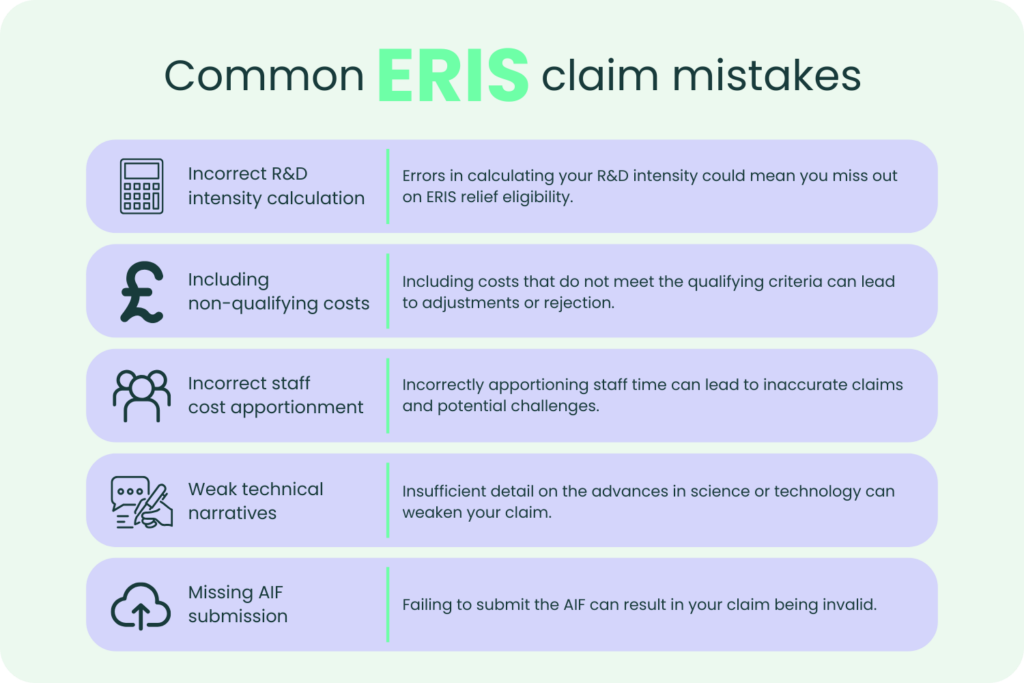

A common mistake is miscalculating the 30% R&D intensity threshold. Businesses must assess their position carefully, particularly where connected companies or wider group structures exist. Claiming under ERIS when the conditions are not met can lead to HMRC challenges or rejection.

Companies should carefully review how grant funding interacts with their claim calculations, particularly where different funding arrangements apply.

Cost Calculation Mistakes

Many claims include costs that no longer qualify under R&D legislation. For accounting periods beginning on or after 1 April 2024, overseas subcontractor and EPW costs are generally excluded unless a specific exception applies.

Businesses also frequently include capital expenditure or fail to apportion staff costs correctly. HMRC expects claims to reflect the actual time employees spend on qualifying R&D activities.

Compliance and Filing Issues

Administrative errors can invalidate an otherwise valid claim. The Additional Information Form (AIF) must be submitted before the CT600. First-time claimants may also need to submit a Claim Notification Form within the relevant deadline.

Technical narratives are another common weak point. HMRC expects companies to explain the scientific or technological uncertainties faced, the work undertaken to resolve them and why the solution was not readily deducible by a competent professional.

Closing thoughts

At Alexander Clifford, we help businesses understand both the ERIS and merged R&D schemes, assess eligibility and prepare evidence-led claims. Our team works with companies to identify qualifying expenditure, evaluate technical eligibility and prepare the documentation required to support a claim.

A successful R&D tax credits claim requires more than just identifying innovative work. It must be accurate, well-evidenced and aligned with HMRC’s expectations from the outset.

We focus on identifying R&D projects that seek an advance in science or technology, establishing the relevant baseline knowledge and developing clear technical narratives that demonstrate how scientific or technological uncertainties were addressed and what the business encountered in the attempt to resolve them.

If you require further clarification regarding the ERIS scheme, please don’t hesitate to get in touch with a member of our team today.