In past R&D legislation, UK companies could include certain overseas subcontractor costs in their R&D tax relief claims. Many projects relied on specialist teams or testing facilities abroad if they were unable to complete the work within the UK. The 2024 R&D reforms changed this position. For accounting periods starting on or after 1 April 2024, subcontracted R&D activity and externally provided worker (EPW) costs must generally relate to work carried out in the UK for the expenditure to qualify for R&D tax relief.

There are limited exceptions where overseas work is necessary due to conditions that cannot be replicated in the UK. Businesses that rely on international R&D assistance should understand how the new rule affects qualifying R&D activity and eligible expenditure.

In this article, we explain the overseas subcontractor rule changes, when they were introduced, and how they have affected R&D tax credit claims across the UK. It also explains how subcontractor costs for work carried out inside and outside the UK are now considered when determining whether expenditure may qualify for R&D tax relief.

What have been the key changes to the R&D claiming process?

HMRC introduced a new territorial approach to R&D tax relief. The focus is now firmly on R&D activity performed in the UK.

The core rule

Under the updated eligibility criteria, subcontracted R&D activity must generally be undertaken in the UK to qualify for Research and Development tax relief.

This applies when:

- A company subcontracts R&D work to a third party, or

- A company incurs externally provided worker (EPW) costs.

If the qualifying activity takes place outside the UK, the cost will generally not be treated as eligible expenditure for an R&D claim.

Impact on subcontracted R&D

Companies could previously claim a proportion of subcontracted costs regardless of where the R&D activity was undertaken, provided the project met HMRC’s definition of R&D and addressed scientific or technological uncertainty the business encountered during the work. The new rules introduced a geographic requirement into R&D tax relief eligibility.

To qualify, the R&D activity must now be:

- Physically carried out in the UK, and

- Directly related to resolving a scientific or technological uncertainty.

For example, a UK engineering firm subcontracting prototype testing to a UK laboratory can still include the cost. The same work carried out by a laboratory in Germany or India would generally fall outside the eligibility criteria.

Documentation expectations

These legislative changes also increase the importance of clear supporting documentation.

Companies should now be able to demonstrate:

- Where the R&D activity took place

- Who carried out the work

- Whether the work was overseen by a competent professional

- How the R&D activity contributed to resolving the technical uncertainty

This information will often appear in the Additional Information Form (AIF) submitted alongside an R&D claim.

Supply chain review

Businesses will need to carefully review their existing supplier arrangements to ensure they remain aligned with the R&D tax relief eligibility requirements.

Key questions include:

- Is the subcontractor undertaking qualifying R&D work?

- Where are their staff physically located when conducting the work?

- Could the work reasonably be undertaken in the UK?

If a project relies on overseas support to resolve scientific or technological uncertainties, that expenditure may now fall outside the scope of an R&D tax relief claim.

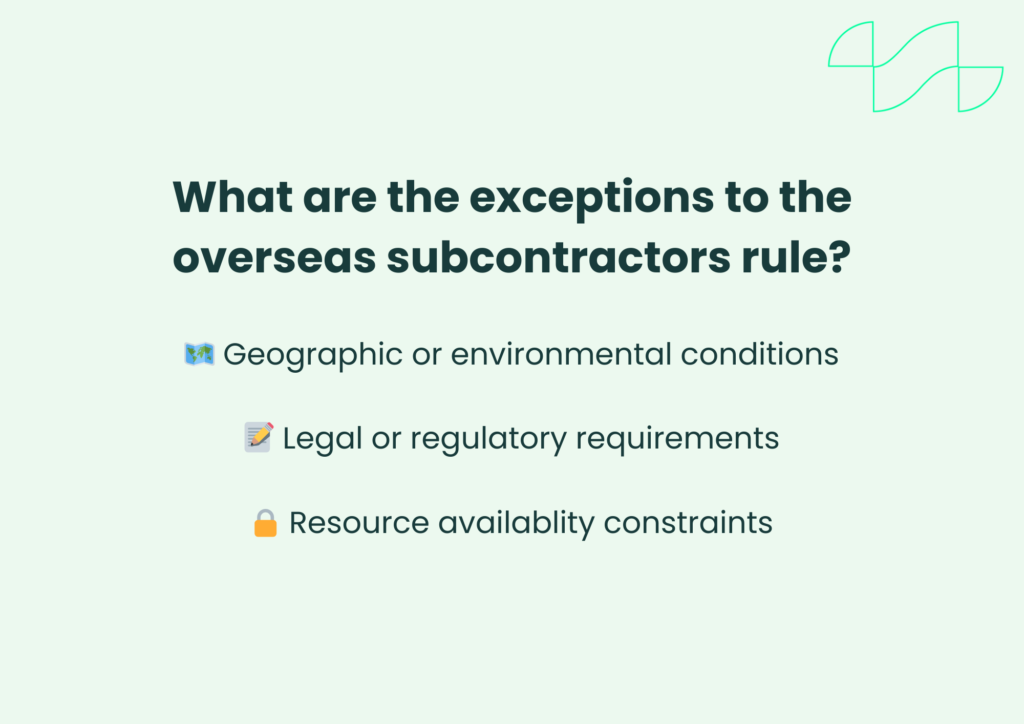

What are the exceptions to the overseas subcontractors rule?

The R&D tax relief legislation recognises that some R&D work cannot reasonably take place in the UK. In these circumstances, overseas activity may still qualify. These exceptions are intentionally narrow and apply only where the conditions required for the R&D activity cannot reasonably be replicated in the UK.

1. Geographic or environmental conditions

An exception may apply if the physical conditions needed to carry out the R&D work are unavailable to source within the UK.

Examples of this include:

- Testing equipment in extreme climates

- Research that requires specific geological conditions

- Environmental testing that depends on unique natural features

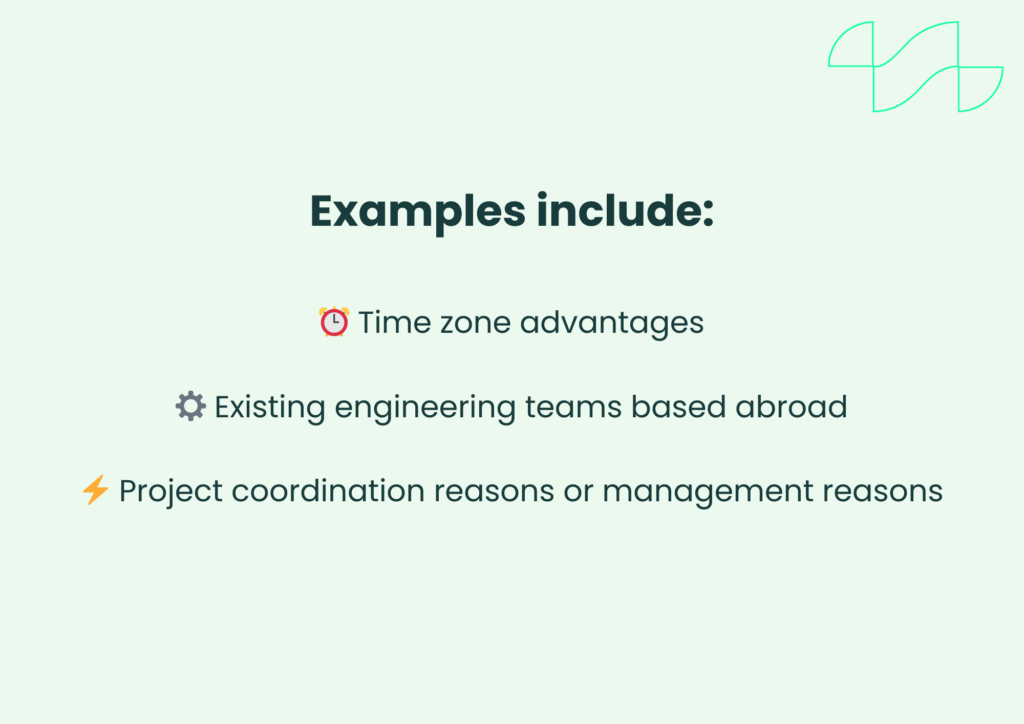

For instance, a company developing geothermal drilling technology may need to conduct trials in locations that have naturally occurring high-temperature geothermal reservoirs. If those conditions are required to resolve the technological uncertainty and are not present in the UK, the overseas work could potentially still qualify as eligible R&D activity.

2. Legal or regulatory requirements

An exception may apply where regulatory requirements mean the R&D work has to be carried out in a specific country outside the UK.

Examples of this include:

- Clinical trials required by a local regulatory authority

- Certification processes required for entry into a specific sector

- Testing that must be carried out abroad to obtain approval of a product

In these situations, the location is dictated by law or regulation rather than the business’s commercial preference.

3. Resource availability constraints

A further exception may apply where the necessary facilities, materials, or population groups cannot reasonably be accessed or replicated within the UK.

Examples could include:

- Specialist testing equipment that is only available overseas

- Research that involves rare materials sourced in another country

- Trials that require access to specific patient populations

In these circumstances, the company would need to demonstrate that the relevant conditions required for the R&D activity could not reasonably have been replicated in the UK.

Evidence expectations

To qualify for an exception allowing overseas subcontractor costs, companies must be able to clearly demonstrate:

- The overseas work directly relates to the qualifying R&D activity

- The location was required due to external constraints

- The work could not reasonably have taken place in the UK

This will typically require clear technical explanations from the competent professionals leading the project, supported by documentation describing why the activity needed to take place overseas.

What is not an exception?

Some scenarios that previously justified overseas subcontracting costs no longer qualify under the new overseas R&D subcontractor rules. Companies need to understand these requirements when preparing an R&D claim.

Lower labour costs

Choosing an overseas contractor because the work is cheaper does not qualify as an exception when claiming R&D tax relief. Cost efficiency alone does not demonstrate that the work could not reasonably be performed in the UK.

Existing supplier relationships

Long-standing supplier relationships also do not meet the exception criteria of qualifying R&D overseas subcontractor costs. Even if a company has previously used a particular overseas specialist, the costs may still be excluded if similar capabilities are available within the UK.

Convenience or project management

Commercial or operational convenience is not a valid reason for overseas subcontracting.

The legislation focuses on whether the R&D activity had to take place overseas, rather than the business’s commercial preference.

Internal group structure

In previous years, there were corporate groups who carried out R&D activity through overseas subcontractors or related group entities.

However, under the recent legislative changes, these arrangements do not automatically qualify. If the R&D activity takes place outside the UK and no exception applies, the expenditure will typically not qualify for R&D tax credits.

Outsourced development teams

Many software and technology companies rely on international development resources. If those external sources perform core R&D activity overseas, the cost will generally fall outside the scope of R&D tax credits unless a valid exception applies.

Why were these changes introduced?

These changes form part of a broader programme to reshape the UK’s R&D tax relief incentives. Several policy objectives informed the introduction of these changes.

Encouraging UK-based innovation

The UK Government continues to encourage innovation activity to be carried out within the UK.

Restricting relief to UK-based activity encourages companies to:

- Conduct research domestically

- Invest in UK laboratories and engineering teams

- Build local technical capability

The policy aims to ensure the tax incentive supports R&D activity taking place within the UK economy.

Addressing compliance concerns

In recent years, HMRC has reported rising concerns regarding incorrect or overstated R&D tax relief claims. Some of these claims included costs that had limited or no connection to genuine scientific or technological advancement. Tightening the treatment of overseas subcontractor activity helps reduce ambiguity in claims and limit opportunities for misallocated relief or incorrect R&D tax credit claims.

Simplifying the scheme

The legislative changes also aim to simplify some areas of the rules for claimants. A clearer geographic framework can be easier to assess than detailed discussions between HMRC and claimants regarding where the R&D activity was undertaken.

While the exceptions can still involve technical interpretation, the main principle of this new requirement is straightforward. Where Research and Development activity carried out in the UK may qualify, overseas activity generally will not qualify unless a specific exception applies.

Supporting the wider R&D strategy

This rule change aligns with the wider UK innovation strategy, including investment in research clusters, universities, and advanced manufacturing. The intention is to ensure that the R&D tax relief system supports activity that contributes directly to the UK economy.

Practical considerations for claimants

Companies preparing an R&D claim should review several areas to ensure the submission aligns with HMRC criteria before it is submitted.

Project planning

Location is an important factor to consider at the project design stage. Businesses should consider where scientific or technological activity will take place before engaging subcontractors.

Contract structures

Some contracts may require additional review to clarify:

- Where the R&D activity is carried out

- Who is responsible for the qualifying R&D activity

- Whether the subcontractor’s work contributes to resolving scientific or technological uncertainty

Evidence gathering

Companies should maintain clear records showing:

- The technical baseline knowledge at the start of the project

- The uncertainties faced by the competent professional leading the work

- The specific scientific or technological activities undertaken to resolve those uncertainties

The business may also need to provide evidence of the location where overseas subcontractors carried out the work.

Reviewing existing claims

Companies that have relied heavily on overseas development teams in past R&D tax credit claims may see reduced claim values under the new rules. Reviewing existing R&D claim documentation in advance can help identify potential risks when preparing the next submission. It may also provide insight into the type of technical and financial information HMRC expects to see within a claim.

Closing thoughts

The updated rules around overseas subcontractors and R&D tax credits represent a shift toward a more territorially focused incentive. For companies engaged in complex development projects, this means taking a closer look at where technical work is actually carried out.

The change does not remove the value of the scheme. UK-based innovation continues to be supported through SME R&D relief, RDEC, and the newer Merged R&D Scheme. Understanding the rules before starting a project can help prevent unexpected issues later in the claim process. For businesses planning significant development activity, reviewing subcontractor arrangements early is now an important step in preparing an R&D tax relief claim.

At Alexander Clifford, we support businesses across the UK in preparing and reviewing R&D tax relief claims across a range of industries. From MedTech to construction, our 5-star rated advisers work with companies to navigate the technical and compliance requirements involved in R&D claims. If you would like to learn more about whether your project may qualify for R&D tax credits, you can contact our team or download our free e-Book covering the key stages of the R&D claim process.