Following a recent conversation with HMRC, we’ve produced this article outlining the spring 2026 updates affecting R&D tax relief claims, with particular focus on the new Advance Assurance Pilot. This guide sets out the key areas you need to know before the official launch.

Some topics covered in this guide are:

- How the Advance Assurance Pilot operates in the R&D claims process

- Where it fits within the wider R&D claims process

- The changes we know so far that have been made

Rumoured to begin around early May, HMRC’s updated Advance Assurance Pilot is intended to improve certainty within the UK’s R&D tax relief framework by allowing companies to seek an early view on whether specific activities meet the definition of qualifying R&D. What businesses needed to know most was if this approach is going to resolve the current limitations of the existing Advance Assurance process.

What is the new targeted Advance Assurance Pilot?

Last year’s budget introduced plans to trial a more “targeted” approach to the Advance Assurance Pilot for R&D tax credit claims in 2026.

During the presentation, they outlined the areas that have been improved such as the eligibility to apply, participants of the pilot can seek assurance on concerns they may have, and an overall improvement of the scheme’s purpose.

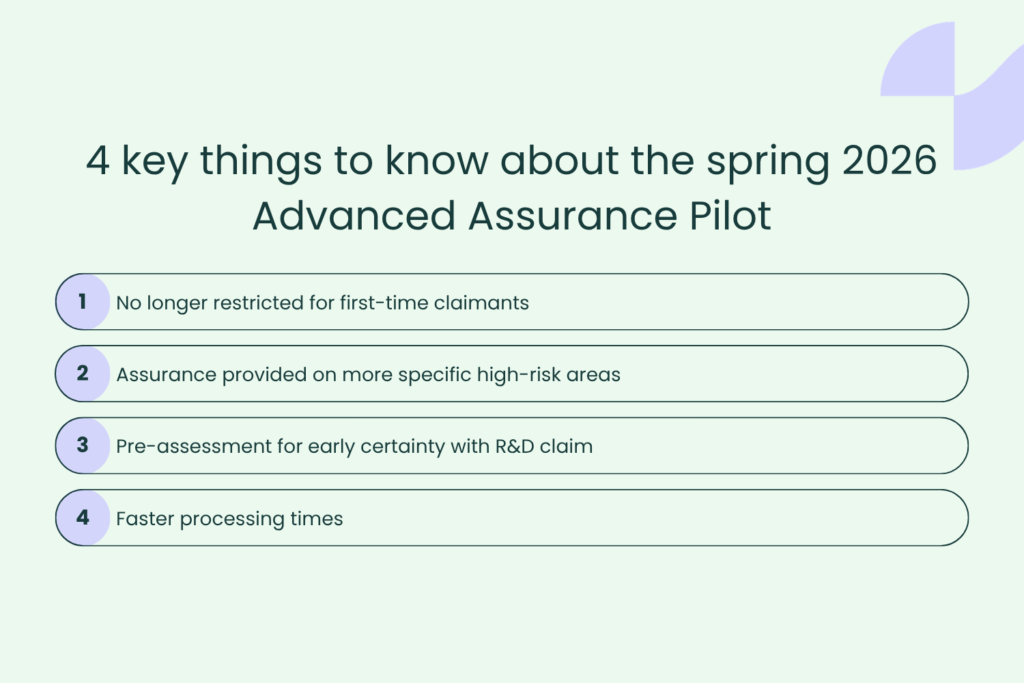

The 2015 pilot scheme is restricted to first-time claimants only. The Spring 2026 pilot will expand access so that a broader range of SMEs can benefit from this process rather than limiting it to first-time R&D tax relief claimants.

Where HMRC provides Advance Assurance on specific technical areas, this can reduce the likelihood of an enquiry being opened, provided that the claim is submitted on a consistent basis. However, it is important to understand that this update does not remove the possibility of HMRC reviewing the claim.

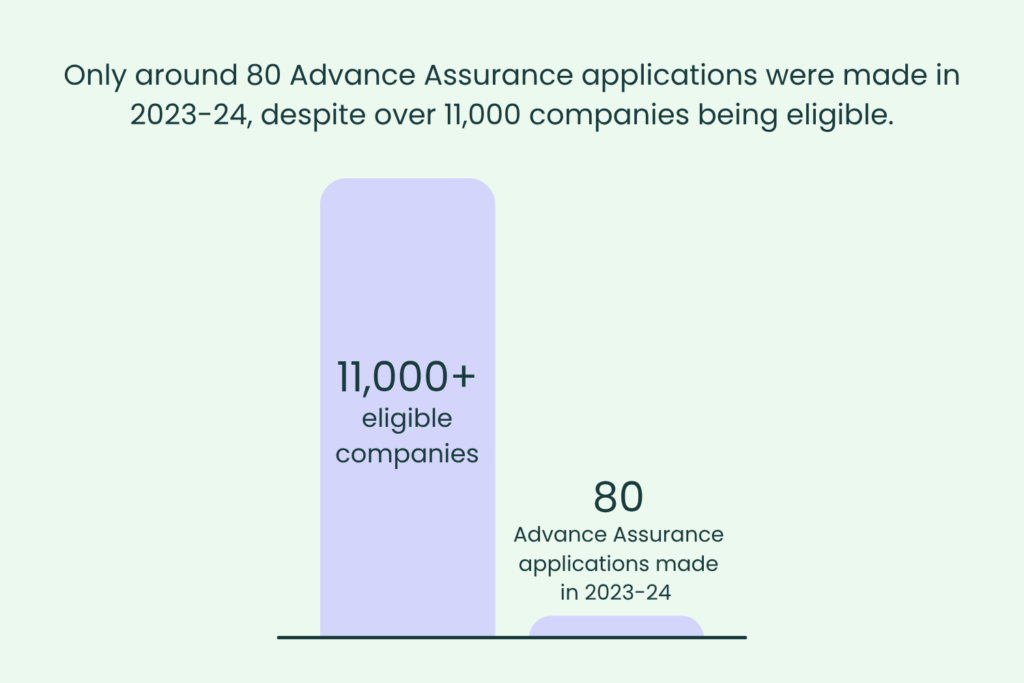

Despite efforts to streamline the process for first-time claimants, 2023-24 statistics show low figures in participation. Out of approximately 11,500 eligible first-time SME claimants during this period, only around 80 companies applied. That’s a participation rate of under 1%.

These statistics raise the question: why has this scheme struggled since launching in 2015?

How has the existing scheme struggled since its introduction in 2015?

A duplication of effort

Applying for the Advance Assurance scheme requires companies to prepare detailed technical and financial information, this is similar to the R&D tax relief claim process itself. For many SMEs, particularly those already working with R&D tax credit advisers, this can feel repetitive rather than supportive.

A Lack of awareness

A significant percentage of eligible SMEs may not know the scheme even exists. Despite being around for several years, it has not been widely embedded into standard R&D tax credit claim processes or consistently promoted as part of HM Revenue & Customs compliance criteria.

Cautious of increased scrutiny

Some companies are reluctant to engage before submitting a claim. There are some concerns that early contact could increase the chance of a compliance check.

Restrictive eligibility

As outlined above, the 2015 scheme is only available for SMEs who are first-time claimants. This means that companies with previous claims are excluded from the existing process. However, when the new Spring 2026 pilot comes into practice, the eligibility is expanding meaning more SMEs can take part.

At the core of this concern is a structural challenge that the new Advance Assurance Pilot must address if it is to succeed in the long term. R&D tax relief relies on being able to demonstrate an advance in science or technology through the attempt of a resolution of scientific or technological uncertainty, based on what a competent professional could achieve using existing baseline knowledge.

What happens during an enquiry?

An R&D enquiry is an in-depth review of a submitted R&D tax relief claim. The review will assess whether the claim reflects qualifying R&D activity, if there was genuine scientific or technological uncertainty, and the costs included are classed as eligible expenditure.

The process often involves detailed questions and requests for additional evidence to support the submitted R&D tax relief claim. The aim of an enquiry is to establish whether the activities described would be recognised by a competent professional as contributing to an advance in science or technology, beyond the existing baseline knowledge.

In cases where the technical narratives are unclear, HMRC enquiries can become prolonged. Requests for further evidence aren’t unusual, especially where the alignment between the work carried out and the definition of qualifying R&D is not clear to the reviewer.

Why is user feedback important for building the new Spring 2026 Advance Assurance Pilot?

For the new Advance Assurance Pilot to be effective for SMEs, it will need to provide a clear and consistent framework for those utilising the scheme. However, if the same structural issues continue from the 2015 model, then the pilot risks repeating the same concerns that led to low engagement and limited practicality.

What would make the 2026 pilot work more efficiently?

For the Spring 2026 Pilot to succeed and provide value to SMEs, there are several areas of feedback from businesses and advisers familiar with the 2015 scheme.

HM Revenue & Customs’ decision to implement a greater emphasis on technical scrutiny within the R&D tax relief process includes clearer identification of qualifying R&D activity and more consistent interpretation of claims. By defining the scope of submissions further and focusing more attention on areas such as overseas expenditure and contracted R&D, HMRC are targeting parts of R&D claims that carry higher compliance risks.

This introduces an optional step before filing. In practice, its intention is to support the preparation of a research and development tax relief claim rather than operate as a separate process. If approached correctly, this pilot could help structure the claim more clearly, support a more straightforward path to submission, and reduce the risk of enquiry.

Setting realistic timelines is an important area to take into account when implementing the new Advance Assurance Pilot scheme. If this process takes too long to deliver, it could very quickly become impractical for businesses.

Embedding technical expertise is a vital component of making the Spring 2026 pilot effective. The process would benefit from input from competent professionals such as engineers, scientists or software specialists alongside R&D tax credit advisers.

This would improve:

- The consistency and credibility of HMRC’s decisions

- Alignment with how R&D is assessed in tribunal cases

- Increase confidence among R&D tax relief claimants using the pilot

If a company has clarity on which aspects of the claim may be reviewed, what level of detail is expected and whether the outcomes are indicative rather than binding, it supports a more predictable process and greater confidence in how the claim is assessed.

Improving accessibility and awareness of the new 2026 pilot will also benefit businesses for future R&D tax relief claims made. HMRC will need to communicate clearly how the pilot operates and what has changed compared to the scheme introduced in 2015.

Should companies wait for the pilot?

For many companies across the UK, choosing whether to wait for the new Spring 2026 Advance Assurance Pilot will depend on their individual circumstances. While the pilot is expected to expand the current process, there are still uncertainties to consider before relying on it.

Reasons include:

- It has not yet launched and an official date is to be confirmed

- The full eligibility criteria has not been formally revealed

- The effectiveness of the pilot remains untested

While the Spring 2026 Advance Assurance Pilot scheme has not begun, companies can continue to submit claims through the existing R&D claims process. The existing Advance Assurance Pilot remains available if the claim is eligible and focuses on strengthening the technical narrative and supporting documentation.

Waiting for the launch of the new Spring 2026 pilot scheme could unnecessarily risk delaying valuable claims. In practice, many businesses continue to submit eligible R&D claims under the current framework without the Advance Assurance Pilot while monitoring further updates regarding this new pilot.

Closing thoughts

HMRC’s new Advance Assurance Pilot scheme for Spring 2026 can become a very useful resource. Until the official launch, we advise you to continue your R&D tax credit journey as normal.

At Alexander Clifford, our team works with UK businesses to prepare and submit R&D tax relief claims that are accurate, well-supported and align with HMRC guidance.

We focus on identifying qualifying research and development activity, assessing technical uncertainty and ensuring that all eligible expenditure is correctly evidenced. Each claim is prepared with care, with input from competent professionals and a clear audit trail.

We understand that approaching R&D tax relief can feel complex. Our role is to provide clear explanations, structured processes and timely responses so clients can make informed decisions with confidence. For more information about claiming R&D tax credits, please get in touch.