Most SMEs misunderstand the qualifying criteria for claiming R&D tax credits. A common misconception is that the project being put forward for claiming R&D tax credits could actually have failed, been put on hold, or the business made a loss during the production of the project. In this article, we are going to be exploring what counts as a technological advancement in R&D tax credit claims.

What does HMRC mean by an advance in science or technology?

At the core of the UK R&D tax relief regime is a requirement that a project seeks an advance in science or technology. This is not optional. Without it, there is no qualifying R&D activity.

HMRC defines as an advance as: “An overall improvement in knowledge or capability in a field of science or technology, not just within the company.”

This leads to two key points.

First, a scientific or technological advancement must go beyond the competent professional’s own baseline knowledge or capability in the field. The R&D activity must aim to resolve the uncertainty that competent professionals in the relevant field could not readily solve.

Second, the advance must be aligned with the scientific or technological criteria to qualify for R&D tax relief. Commercial, aesthetic or operational improvements do not qualify for R&D tax credits unless they are met with a genuine technical challenge. This technical challenge must be well-evidenced within the technical documentation required when submitting an R&D tax relief claim.

How does technological advancement and business innovation differentiate?

A common issue in R&D tax credit claims is the difference between business innovation and technological advancement, it is important to understand that these are not the same.

It is common that businesses might:

- Launch a new product, software or service

- Enter a new market

- Improve their user experience

- Reduce costs or delivery times

These points can all bring commercial value, but on their own they do not meet HMRC’s definition of qualifying R&D activity.

To qualify, the project must seek an advance in science or technology by resolving scientific or technological uncertainty. The key focus relies on the underlying systems, processes or materials. It is not about the commercial result but the resolution of the uncertainty faced across the duration of the work.

An example of this would be if a company was to develop new software where the team is trying to overcome a genuine scientific or technological uncertainty that could not readily be resolved using publicly available knowledge or standard approaches. The distinction of qualifying R&D lies in whether the R&D activity required resolving genuine scientific or technological uncertainty.

What is the role of baseline knowledge?

The criteria for a technological advancement is assessed against the “baseline knowledge” in the relevant field.

Examples of baseline knowledge includes:

- Information that is publicly available

- Industry standards and practices

- Existing technologies and methodologies

Baseline knowledge does not include:

- The company’s internal limitations

- Lack of in-house expertise

- Time or budget constraints

This is where many R&D claims require framing that is closely and carefully examined. A project can be new to a business without being entirely new to the industry that they specialise in. The most important part of this is whether the advance goes beyond what is publicly available or readily deducible by a competent professional.

Why is scientific or technological uncertainty required for R&D tax relief?

Scientific or technological advancement cannot exist without uncertainty. Under the official criteria, HMRC describes scientific or technological uncertainty as an area where a competent professional cannot readily determine whether a solution is possible, or how to achieve it using current knowledge.

Indicators of scientific or technological uncertainty include:

- Inconsistent results from existing methods

- No clear or documented solution within current knowledge

- Existing technologies cannot meet the performance levels required for the project

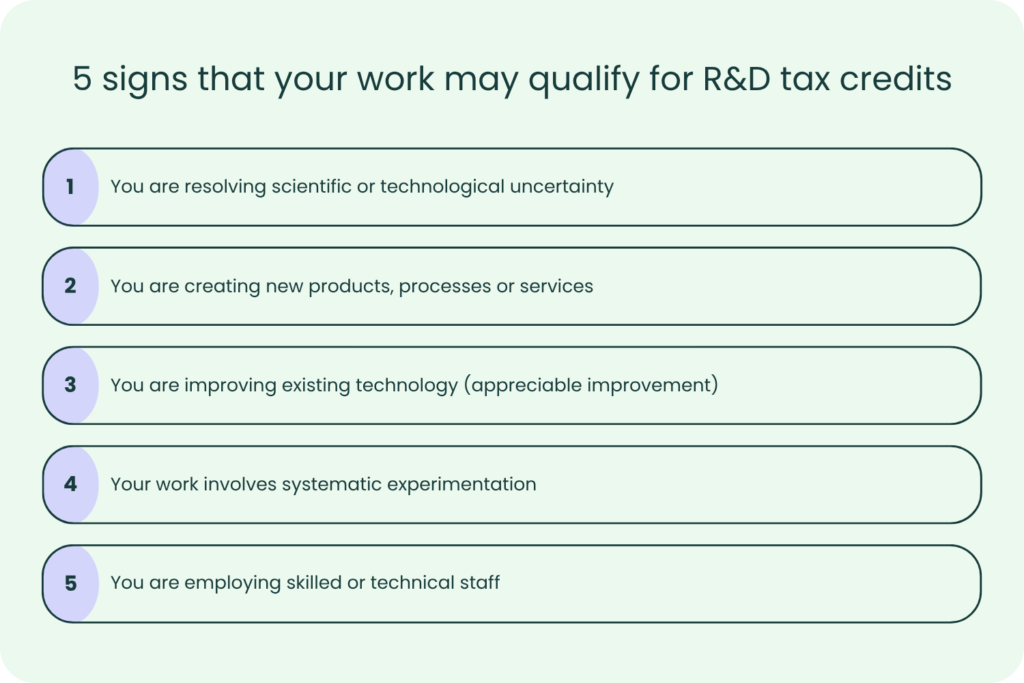

What does an “advance” look like in practice?

HMRC does not require a project that is groundbreaking and entirely new. Incremental improvements can qualify if they represent an appreciable improvement in knowledge or capability.

Below, we have listed some common types of qualifying advancements:

1. Performance improvements beyond known limits

Work that increases speed, accuracy or efficiency where existing methods are unable to achieve the target.

2. New or improved processes

Developing a technique that enables something to be done in a way that was not readily achievable using existing knowledge or standard methods.

3. Integration of existing technologies where standard approaches do not work

Combining existing technologies can qualify if the integration itself presents non-trivial scientific or technological challenges.

4. Adapting technology to new contexts

Applying existing technology in an environment where it does not effectively function.

What does not count as a scientific or technological advancement?

Technical documentation is important where a company needs to explain why work did or did not qualify, including where a project was unsuccessful.

The following activities do not typically qualify as a genuine technological advancement:

- Routine software development using established tools

- Cosmetic or user experience improvements

- Data or system upgrades without facing any scientific or technological uncertainty

- Trial and error without a clear scientific or technological objective

These activities may form part of a wider project, but they must be separated from the work that qualifies for R&D.

What is the role of the competent professional?

The role of the competent professional in an R&D claim is the central focus point for assessing both scientific or technological uncertainties and advancements.

A competent professional is the main person who will:

- Have relevant qualifications or experience

- Understand the current state of knowledge in the field

- Identify whether a solution is readily deducible

This benchmark prevents R&D tax relief claims from relying on in-house skill gaps. When preparing an R&D claim, it is useful to frame the technical narrative around what a competent professional would have known from the beginning, and why the solution was not obvious.

How would a business demonstrate a scientific or technological advancement?

HMRC expects R&D tax credit claims to be supported by clear, contemporaneous evidence where possible. Estimates and unsupported assertions are not enough on their own, and should be supported by technical justification to reduce the risk of enquiry.

Examples of effective evidence include:

Technical narratives

- The starting point (baseline knowledge)

- The scientific or technological uncertainties faced

- The work undertaken to resolve these uncertainties

- The outcome and how it advanced capability

Development records

- Design documents

- Test plans and results

- Iteration logs

- Technical discussions or decision records

Finally, the company should input details of the roles of engineers, developers or scientists involved in resolving the scientific or technological uncertainty. The aim of this demonstration is to show a clear, logical progression of identifying an uncertainty within the process of the project and working towards a resolution.

The solution does not have to be successful. What matters is that the work undertaken to resolve a genuine scientific or technological uncertainty and ensuring it is supported by clear evidence.

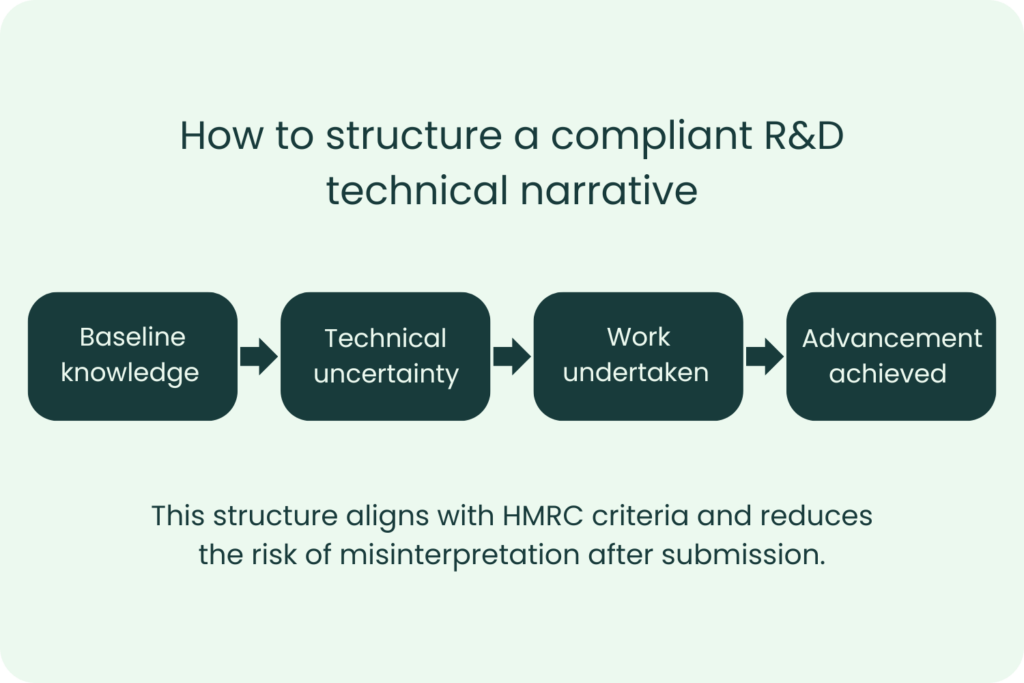

What is the best way to structure the narrative in an R&D claim?

Compliant R&D technical documentation should clearly display the technological advancement in a structured way. A typical framework example is:

- Baseline knowledge of technology

Apply the knowledge that was already available in the field. - Scientific or technological uncertainties

Explain why the uncertainty could not be readily resolved by a competent professional using available knowledge. - Work undertaken

Explain the systematic process of experimentation or development. - Scientific or technological advancement achieved

Show how the research and development activity undertaken extended existing knowledge or capability.

Common risks in claims

There are several recurring issues that lead to risking an HMRC enquiry:

- Misinterpreting routine work as R&D activity

- Failing to distinguish between business and technological objectives

- Lack of clarity on baseline knowledge

- Insufficient evidence of scientific or technological uncertainty

- Describing the resolution without explaining the technical journey

These risks can be reduced through careful preparation and an internal review.

Closing thoughts

Scientific or technological advancement, in the context of R&D tax relief, is defined by the underlying science or technology rather than the commercial outcome. A project must seek to extend capability or knowledge within the relevant field, not just within the business. This requires the presence of scientific or technological uncertainty that is not readily deducible by a competent professional. Clear identification of baseline knowledge, careful differentiation of qualifying and non-qualifying R&D activity, and well-structured technical narratives are what builds a strong framework for a compliant and defensible R&D tax credit claim.

At Alexander Clifford, we assess projects across a range of industries against HMRC’s definition of R&D to identify where genuine scientific or technological advancement has been sought. We work with businesses across the nation to define the relevant uncertainties encountered, isolate qualifying R&D activity, and document the work undertaken in a consistent and compliant format.

Our approach focuses on aligning each R&D tax credit claim with HMRC’s criteria, supported by appropriate technical evidence, so that claim submissions clearly reflect the reality of the research and development activity and is defensible against the risk of enquiry.

For more information about what counts as a scientific or technological advancement in an R&D claim, please don’t hesitate to get in touch with a member of our team.