The R&D Claim Notification Form (CNF) is a pre-notification requirement that applies to certain companies seeking to claim R&D tax Relief.

HMRC introduced this requirement as part of its wider compliance requirements to improve claim quality and reduce non-compliant submissions. If a company is required to submit a Claim Notification Form and fails to do so within the statutory deadline, it cannot make a valid R&D tax relief claim for that accounting period.

This article explains when a Claim Notification Form is required, the applicable deadline, and the information HMRC expects companies to provide.

It will cover areas such as:

- What a Claim Notification Form is

- Which companies must submit one

- The deadline for submission

- The information required

What is a claim notification?

A claim notification is the formal process of informing HMRC that a company intends to submit an R&D tax relief claim. Companies must notify HMRC by submitting a Claim Notification Form, also known as a CNF. Where required, the company must submit the form through HMRC’s online service within six months of the end of the relevant accounting period.

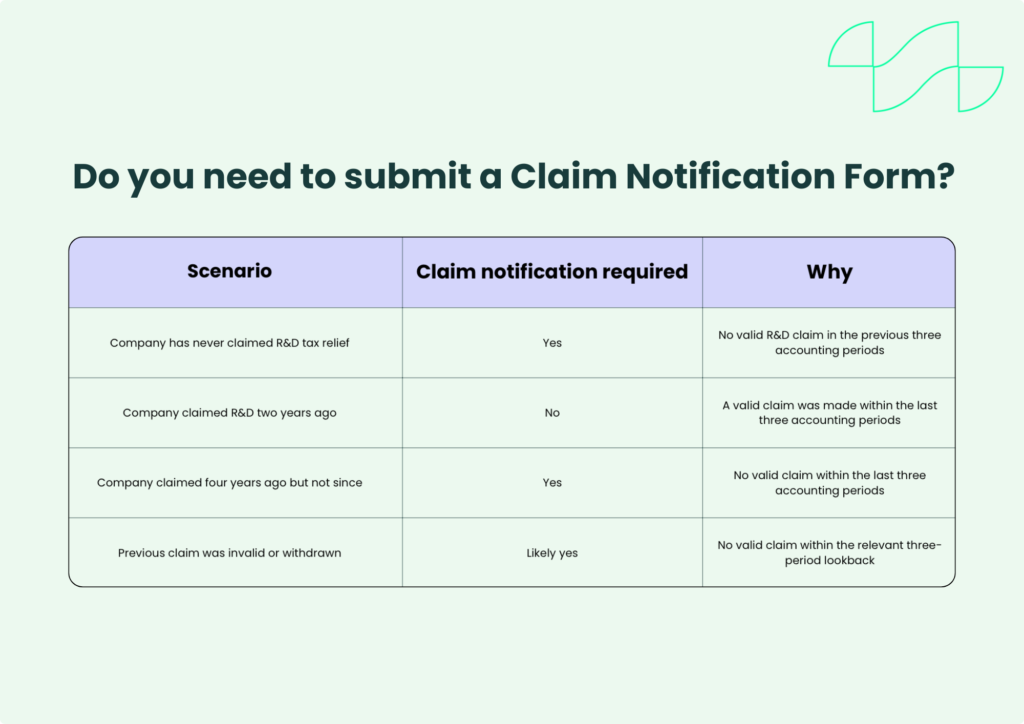

It is important to note that the CNF is not the R&D claim itself, it is a gateway requirement that applies where a company has not made an R&D tax relief claim in any of the previous three accounting periods. If this notification is missed, the company cannot make a valid R&D tax relief claim for that period.

Who needs to submit a Claim Notification Form?

A company must submit a Claim Notification Form if:

- It intends to claim R&D tax relief for the accounting period of which R&D tax relief activity was undertaken, or

- It has not made an R&D tax relief claim in any of the previous three accounting periods.

What is the deadline?

The claim notification must be submitted to HMRC within six months of the end of the accounting period for which the company intends to claim R&D tax credits.

For example, a company’s accounting period ended on 31 December 2025. The claim notification period runs from 1 January 2026 to 30 June 2026. The company intends to make its first claim for R&D tax relief for the accounting period ending 31 December 2025. It will have until 30 June 2026 to submit a Claim Notification Form to HMRC.

If this deadline is missed, the company cannot make a valid R&D tax credit claim for that accounting period.

What information is required for a Claim Notification Form?

The CNF form is submitted digitally via HMRC’s online service. The form requires the company to provide the following information:

- Company details, including its Unique Tax Payer Reference (UTR)

- Dates of the accounting period for which the R&D tax relief claim will be made

- Contact details of the senior internal R&D contact

- Details of any external agent involved in the claim

- A brief description of the R&D activities undertaken

This description should clearly outline an overview of the project(s).

The explanation should reflect HMRC’s definition of qualifying activity based on the guidelines provided.

How do I submit my R&D Claim Notification Form?

Step 1: Find the Claim Notification Form on HMRC’s website

The R&D Claim Notification Form is available on GOV.UK and must be completed online through the company’s Government Gateway account. The company will need its login details ready. If these are not in place, it must register before accessing the form.

Step 2: Confirm that the business is required to notify HMRC

Before starting the form, the company must confirm that a Claim Notification Form is required. A claim notification is needed where the company intends to claim R&D tax relief and has not made a valid R&D claim in a Corporation Tax return in any of the previous three accounting periods. If a valid R&D claim has been made within that timeframe, a notification is not required.

Step 3: Prepare the required information

Next, the company must complete each section of the online form and ensure the information entered aligns with the relevant accounting period and company records.

Accounting period dates, company details and any agent information must be disclosed accurately. Errors at this stage of the submission process may result in follow-up queries from HMRC or delay the claim process.

Step 4: Submit the Claim Notification Form within the six-month deadline

The form must be submitted within six months of the end of the accounting period for which the R&D tax relief claim will be made. The company should retain confirmation of submission for its compliance records. Missing the deadline prevents the company from making a valid R&D claim for that accounting period.

Completing these steps carefully reduces the risk of error and supports a valid R&D tax relief claim.

What are the benefits of notifying HMRC early?

Informing HMRC of a claim notification in good time helps ensure the statutory deadline is met and reduces the risk of losing entitlement to claim R&D tax credits for that accounting period.

These are some practical reasons to consider early submission:

Early planning- Allows more time to prepare structured documentation and ensure the claim is supported by accurate records that reflect qualifying R&D activity and eligible expenditure.

Tax position- Supports timely access to R&D tax relief where qualifying activity and eligible expenditure are present.

Completing the Claim Notification Form- Provides certainty that the company has met the notification requirement and can proceed with submitting an R&D tax relief claim within the statutory timeframe.

Strategic planning- Allows the company to align its R&D claim with budgeting, cash flow forecasting, and resource allocation.

What are some common errors in Claim Notification Forms?

Certain errors frequently arise during the Claim Notification Form process. Some of these errors include:

- Missing or incomplete information

- Incorrect company or contact details

- Missing the six-month notification deadline

- Providing an unclear or insufficient description of the R&D activities

- Mismatched accounting periods

- Misunderstanding eligibility under the R&D tax relief rules

- Inconsistent information compared with the Corporation Tax return

Errors in the Claim Notification Form may result in follow-up queries from HMRC or delay the claim process. In areas where the notification requirement is not correctly completed or submitted on time, the company will not be able to file a valid R&D tax relief claim for that accounting period.

What are the risks of submitting a claim without notification?

Serious consequences can arise if a business fails to notify HMRC regarding the intention to claim R&D for tax purposes.

This may result in:

- Not being able to make the claim

- Increased scrutiny for the duration of the tax return process

- Encountering delays during the claiming process

HMRC are continuing to tighten their guidelines for claiming R&D tax relief and cracking down on incorrect and non-compliant claims, so it is crucial that a company follows these guidelines correctly and chooses the appropriate advisers that will help to get the best possible results from the R&D claim.

Failing to submit an R&D claim without the Claim Notification Form, could trigger a deeper HMRC investigation. This could include:

- A detailed enquiry into the company’s R&D activities and Corporation Tax treatment

- Requests for supporting technical or financial documentation

- Consideration of R&D claims that were submitted in appropriate previous accounting periods

Without a valid claim notification, HM Revenue and Customs may reject the claim regardless of eligibility or return the R&D tax credit claim for correction which could significantly delay the process.

Non-compliant Research and Development claims could also lead to financial penalties.

Penalties may include:

- Loss of entitlement to R&D tax relief for the relevant accounting period where statutory requirements have not been met

- Interest charges on any underpaid Corporation Tax

- Financial penalties where inaccuracies are found to be careless or deliberate

In cases that involve deliberate behaviour, higher penalties may apply.

How can these errors be avoided?

The most effective way to avoid Claim Notification Form errors is to cautiously review all information carefully before submission. This is a key opportunity to check that company details, accounting period dates and contact information consistently align with the company records, and that the claim notification is required based on the company’s previous three accounting periods.

Submitting the claim notification in good time within the six-month statutory deadline allows time to review and correct any incorrect information. Companies should also ensure that the technical description of the R&D activities reflects HMRC’s definition of qualifying activity and aligns with the relevant accounting period for which the claim will be made.

Careful preparation and submitting the notification in a timely manner will help reduce errors and allow the business to make a valid R&D tax relief claim.

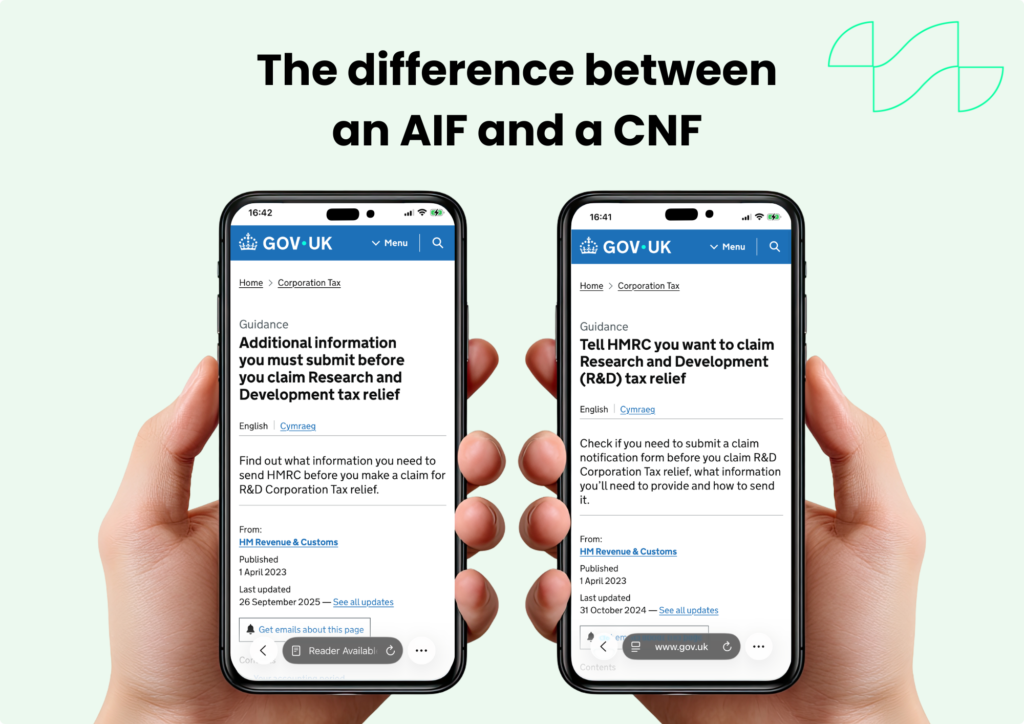

What is the difference between a CNF and an AIF?

There is often confusion regarding the differences between the Claim Notification Form (CNF) and the Additional Information Form (AIF).

A Claim Notification Form is a formal online submission to inform HMRC that a company intends to make an R&D tax relief claim for the relevant accounting period. A CNF is only required where the company has not made a valid R&D tax relief claim in any of the previous three accounting periods.

An Additional Information Form is a part of the R&D claiming process. It is a mandatory digital document submitted to HMRC that provides essential company information, descriptions of R&D activity, and qualifying R&D expenditures. It gives HMRC an indication of whether your project will qualify for R&D tax credits. Without a valid Additional Information Form, the R&D claim will not be accepted.

How does the claim notification interact with the CT600?

The CT600, also known as the Corporation Tax Return, is a formal return submitted to HMRC. It discloses information such as statutory accounts, a detailed tax computation and any relevant supporting financial documentation.

Where the claim notification must be submitted within six months of the end of the relevant accounting period, the Corporation Tax Return is due 12 months after the period ending. These are two different deadlines, so organisation is key.

Even if the CT600 is submitted on time, failure to meet the claim notification deadline will prevent the company from making a validated R&D claim for that accounting period.

Closing thoughts

If the Claim Notification Form is not filed correctly, it can hold clear compliance consequences. Companies must confirm whether the notification to HMRC is required, ensure the information submitted aligns with their CT600 and meets the six-month deadline.

Failure to meet the requirements of a Claim Notification Form can result in invalidating the claim entirely for that accounting period, so it is important that the notification aligns with the company’s R&D activity and planned claim.

At Alexander Clifford, we have the team you need in order to claim R&D in a compliant and timely manner. The team are the brains behind the operation, they dedicate their time and expertise to guide each and every client through the process of claiming R&D.

If you have been seeking expert advice, we are the team for your project. Contact our team to discuss your project today or browse through our previous articles there you will find knowledgeable insights into the world of claiming R&D tax credits, insightful updates, concise information and so much more.