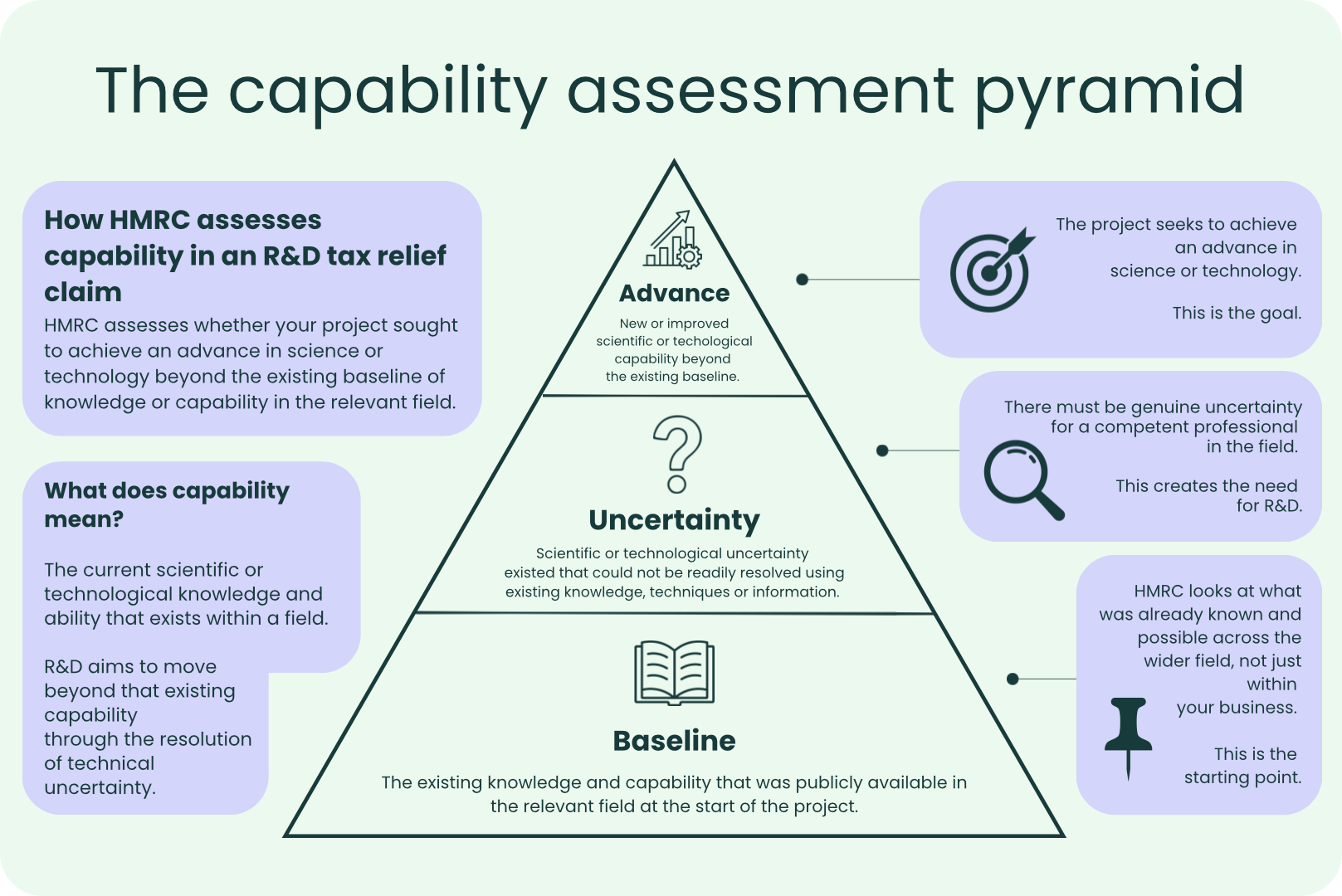

Under HMRC’s R&D tax credits relief guidelines, capability refers to what can be achieved within a field of science or technology using the existing scientific or technological knowledge or methods available at the time. Qualifying R&D projects must seek an advance in the overall knowledge or capability of a field of science or technology, rather than simply improving a company’s own products, processes or internal expertise.

Learning how capability is assessed can help businesses determine whether their projects sought a genuine scientific or technological advance and whether scientific or technological uncertainties had to be resolved during the work.

In this article, we are going to discuss what capability means within the context of an R&D project and how it can influence eligibility for R&D tax relief.

How does HMRC assess capability within an R&D project?

When reviewing an R&D tax relief claim, HMRC does not assess capability from the perspective of that business alone. Instead, they consider whether the activity undertaken sought to achieve an advance in science or technology when compared to the existing knowledge and capability publicly available within the relevant field.

This assessment often focuses on the scientific or technological uncertainty at the outset of the project. HMRC will consider what knowledge and capability already existed within the field and whether the project sought to move beyond those uncertainties.

Businesses should be able to explain:

- What was already known within the field

- What scientific or technological limitations existed

- Why the desired outcome could not be achieved using readily available techniques, technologies or information

- How the project sought to achieve an advance in science or technology

HMRC’s R&D guidelines place particular emphasis on scientific or technological uncertainty. Scientific or technological uncertainty is a key indicator that a project was attempting to achieve an advance in science or technology beyond the existing knowledge or capability within the relevant field.

Where a competent professional could not readily determine how to achieve the intended outcome using existing knowledge, techniques or publicly available information, the project may involve qualifying research and development activity.

Supporting evidence is an important part of the R&D claiming process. Supporting evidence examples include:

- Technical documentation

- Design records

- Testing results

- Meeting notes

- Project reports

These examples all help demonstrate how uncertainties were identified and addressed throughout the project lifecycle and how the work sought to advance scientific or technological knowledge or capability.

An R&D tax relief claim is more likely to be accurate and defensible where the business presents a clear explanation of the scientific or technological baseline, the uncertainties encountered and the work undertaken in an attempt to achieve an advance in science or technology.

Capability and innovation are terms that are often used during business discussions, but they do not necessarily mean the same thing within an R&D tax relief claim.

A project could be classed as innovative where it introduces a new product, service or process. This does not mean it will definitely involve a scientific or technological advance.

HMRC’s assessment focuses on whether a project sought to achieve an advance in science or technology and whether scientific or technological uncertainty existed. Capability forms part of that assessment because it helps establish what was already possible within the relevant field and whether the project attempted to move beyond it.

It is not enough for a product, process or service to be new to a business, sector or market if it can be developed using existing knowledge, established techniques or readily deducible solutions.

If a company launches a software platform which delivers a new customer experience or business model and was created using available technology or standard methods of development, it is unlikely to qualify as genuine R&D.

Why is the competent professional important when assessing capability?

The project’s competent professional must possess the knowledge and experience necessary to understand the scientific or technological challenges involved in the project. Their expertise should be relevant to the field of science or technology in which the work is being undertaken.

If a competent professional could readily determine the solution using existing knowledge, techniques or technologies, scientific or technological uncertainty is unlikely to exist.

Where a competent professional could not readily determine how to achieve the desired outcome using existing knowledge, techniques or available information, the project may involve qualifying R&D activity.

In these circumstances, the business should be able to explain the uncertainties encountered, the work undertaken to investigate possible solutions and how the project sought to achieve an advance in science or technology.

What types of projects may involve scientific or technological uncertainty?

Examples of project types that may involve scientific or technological uncertainties are:

- Achieving a level of performance not previously reached

- Integrating technologies that have not previously worked together

- Developing a new material with specific properties

- Solving complex software scalability issues

How can businesses demonstrate an advance in capability?

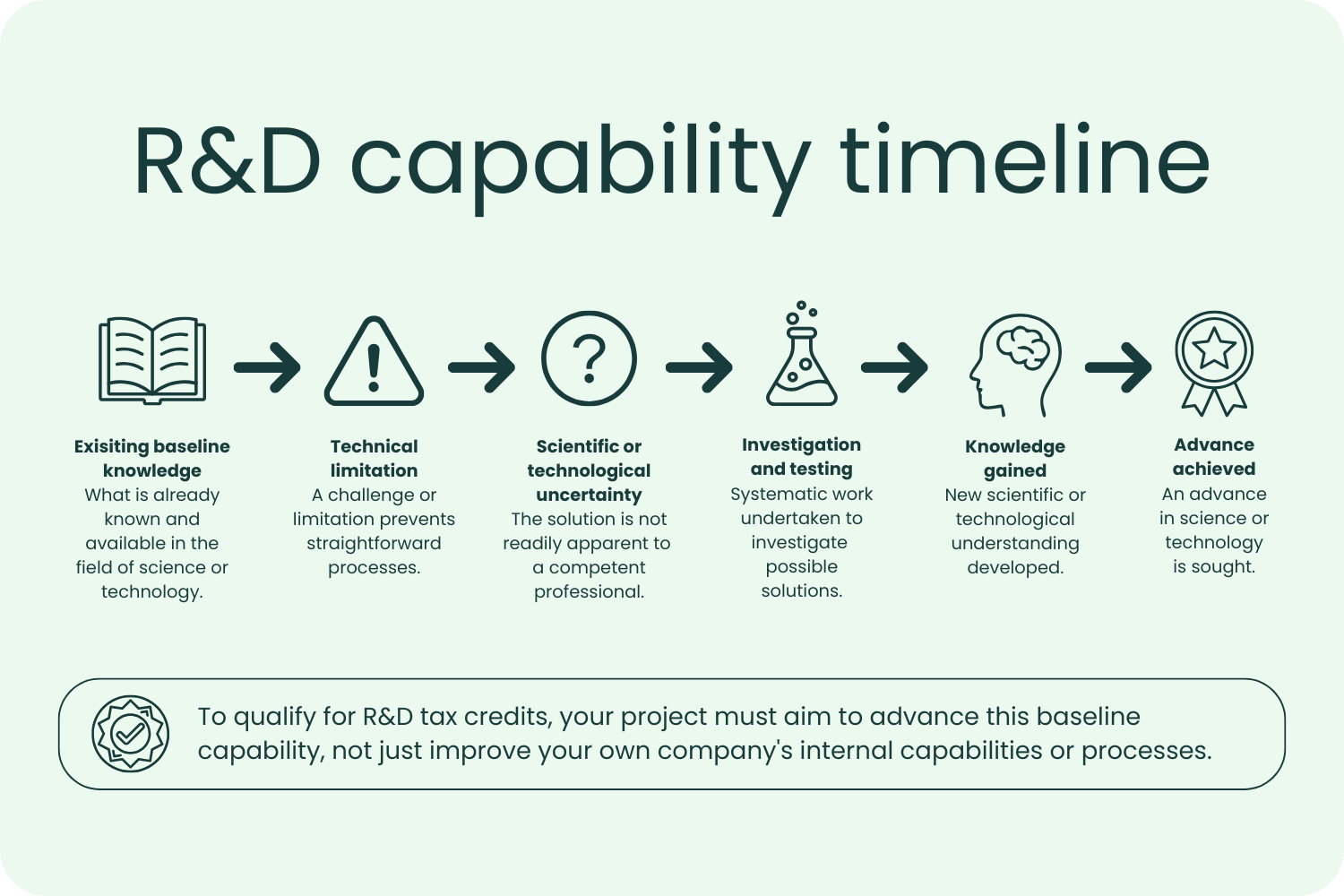

Demonstrating an advance in science or technology requires more than describing the end result of a project. Businesses should be able to show how the work sought to extend scientific or technological knowledge or capability, what uncertainties had to be overcome, and why existing knowledge, techniques or technologies were insufficient to achieve the desired outcome.

This often involves identifying:

- Existing scientific or technological knowledge or capability within the relevant field at the beginning of the project

- Specific uncertainties that prevented straightforward progress to an outcome

- The work that was carried out to investigate possible solutions to the uncertainty

- Testing, experimentation or development activity results

- Knowledge gained during the project, regardless of whether the outcome was successful

Why does capability matter when making an R&D tax credit claim?

Capability is important because it helps businesses assess whether their projects sought an advance in science or technology as defined by HMRC.

When an R&D claim is being prepared, companies should be able to clearly outline areas such as why the solution was not readily deducible by a competent professional and what scientific or technological limitations did the business encounter.

If an R&D claim is supported by appropriate evidence, it helps establish that the work went beyond routine business development and was undertaken to overcome scientific or technological uncertainty.

Is your project eligible for claiming R&D tax credits?

A project might qualify for R&D tax relief if it sought to achieve an advance in science or technology by resolving scientific or technological uncertainty.

To support an R&D claim, businesses should be able to demonstrate that the work aimed to advance the existing knowledge or capability within a field of science or technology.

Eligible projects will clearly demonstrate the following areas:

- There was an aim to achieve an advance in science or technology

- The advance was not readily achievable using existing knowledge, techniques or technologies

- Scientific or technological uncertainties were encountered during the project

- A competent professional could not readily determine a solution at the outset

- Systematic work was undertaken to resolve those uncertainties

The project does not need to be successful to qualify for R&D tax relief. R&D tax relief is intended to support companies undertaking qualifying research and development activities that seek an advance in science or technology through the resolution of scientific or technological uncertainty.

When assessing eligibility, businesses should focus on the scientific or technological uncertainty encountered and explain why a solution was not readily deducible by a competent professional.

Closing thoughts

Understanding capability is an important part of assessing whether a project may qualify for R&D tax relief. HMRC’s focus is not on whether a company developed a new capability internally, but whether the project sought to advance the overall scientific or technological capability within a particular field.

In practice, R&D tax credit claims that clearly demonstrate the existing baseline of knowledge and explain how a project attempted to move beyond it are more likely to align with HMRC’s criteria.

Qualifying claims should show not only that technical work was undertaken, but that the activity was carried out to resolve scientific or technological uncertainty rather than apply existing knowledge, techniques, or technologies.

At Alexander Clifford, we focus on identifying where projects go beyond established capability, defining the technological baseline, and building technical narratives that:

- Clearly explain the scientific or technological challenge

- Demonstrate why the uncertainty could not be readily resolved by a competent professional

- Evidence how the project sought to achieve an advance in science or technology

Our evidence-led and cautious approach helps ensure that each R&D tax relief claim accurately reflects the qualifying activity undertaken, the uncertainties encountered, and the associated expenditure. This allows claims to be both defensible and compliant.

If you require support with assessing whether your project meets the criteria for claiming R&D tax relief, please get in touch with a member of our team.