For companies who are in the process of developing patentable projects, the alignment between claiming R&D tax credits and Patent Box relief is often overlooked. In this article, we are going to discuss how these two reliefs work together in practice, including how claims can be structured in line with HMRC guidelines.

What is the difference between Patent Box and R&D tax relief?

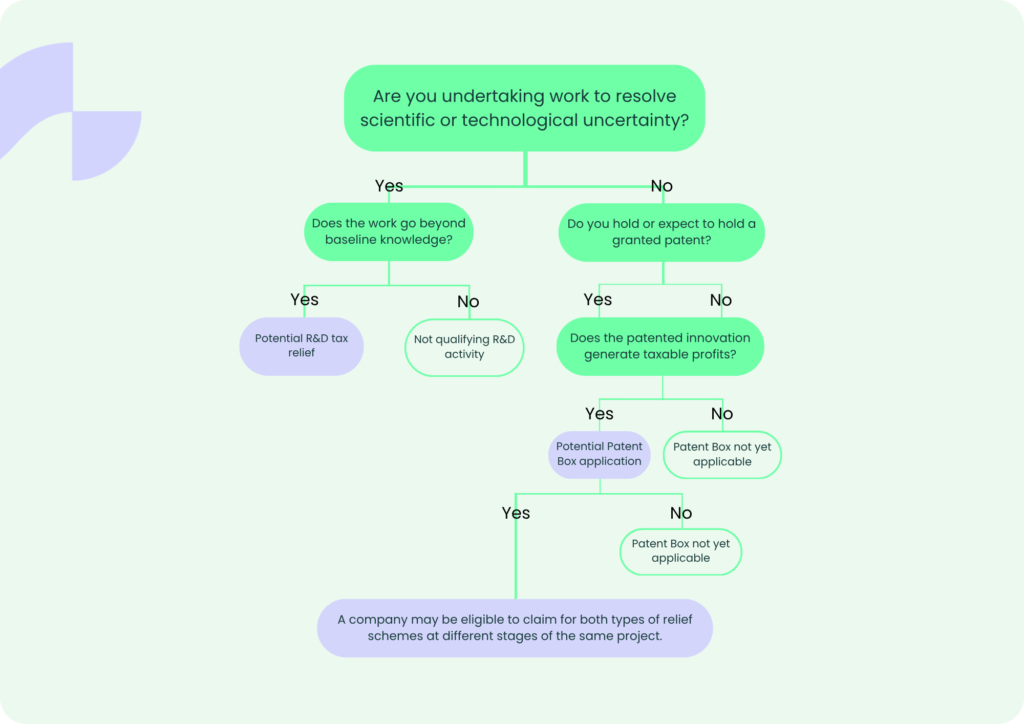

R&D tax relief is a UK government incentive designed to support companies undertaking qualifying research and development activity. It applies to eligible expenditure incurred while resolving scientific or technological uncertainty that could not be readily deduced by a competent professional. This can result in a Corporation Tax Liability reduction/refund or for a loss-making company, a payable credit will be issued.

For accounting periods beginning on or after 1 April 2024, most companies claim under the Merged R&D scheme. Loss-making SMEs that meet the R&D intensity threshold may qualify for Enhanced R&D Intensive Support (ERIS). Eligible companies can claim R&D tax credits whether they are profit or loss-making.

Alternatively, Patent Box is a separate tax incentive scheme. It allows companies to apply a reduced 10% rate of Corporation Tax to profits attributable to patented inventions and qualifying intellectual property. Patent Box relief applies once innovation has moved into commercial use.

R&D tax relief and Patent Box relief both support growth and innovation, but they apply to different aspects of relevant activity and income. While they can be used in combination, they operate at different stages of the innovation lifecycle. R&D tax relief applies on expenditure already incurred by the company during development, whereas Patent Box applies once income is generated from patented outcomes.

How does the Patent Box and R&D tax credit relief link in practice?

In practice, Patent Box relief and R&D tax credits are separate UK tax incentives that apply across the innovative process of a business project.

R&D tax relief reduces the cost of development when a company undertakes qualifying research and development activity to resolve scientific or technological uncertainties.

Patent Box tax relief applies at a later stage, reducing the rate of Corporation Tax on profits attributable to patented inventions once they are commercialised.

Where a business intends to apply for Patent Box relief in the future, it is important that R&D activity is documented in a way that supports a clear link between development work and any resulting intellectual property. This includes maintaining clear project narratives and identifying the scientific or technological uncertainties addressed. It also requires a consistent approach to recording qualifying activity and associated expenditure throughout the development process. Clear documentation clarifies the demonstration of how work has progressed beyond baseline knowledge within the relevant field.

While Patent Box operates separately to R&D tax credits, well-structured R&D documentation can help establish a clear link between development activity and income derived from patented innovation.

What are the differences in eligibility?

There are many differences in these two government relief schemes. Below we have gathered a list of four key eligibility differences to understand:

- Ownership-

Patent Box requires a company to either have ownership or exclusively license the patented invention. The company must also have contributed to the development of the patented project.

R&D tax relief requires ownership of intellectual property. A company can claim for qualifying research and development activity where it incurs eligible expenditure on work not contracted to it by another entity.

- When the relief applies-

R&D tax relief applies to qualifying expenditure incurred during the development phase of a project. Companies can claim whether they are profit or loss-making.

On the other hand, Patent Box relief only applies to projects when the innovation has been granted a patent and is generating income.

- Intellectual property requirement-

R&D tax relief does not require a patent. Eligibility is based on whether the work seeks to achieve an advance in science or technology and involves resolving technical uncertainty.

When claiming Patent Box relief, one of the main requirements within the eligibility criteria is to have a granted patent. Patents are typically granted by the UK Intellectual Property Office (UKIPO) or the European Patent Office.

- Scope-

Patent Box applies to profits generated from patented inventions. This can include licensing income, infringement income and sales, provided the business meets the relevant criteria.

R&D tax relief applies to qualifying R&D activity, including projects that may be unsuccessful, abandoned, or still in development. The eligibility criteria for claiming R&D tax relief states that the eligibility depends on the attempt to achieve an advance in science or technology.

Can a business claim both types of relief?

Yes. A business can claim both types of relief, provided the criteria for each scheme are met.

R&D tax relief applies to qualifying research and development activity and eligible expenditure incurred in resolving scientific or technological uncertainty. Patent Box applies at a later stage, reducing the rate of Corporation Tax on profits attributable to patented inventions.

While both schemes can relate to the same underlying innovation, they operate differently and must be calculated separately within the tax computation. Providing clear, evidenced documentation of qualifying R&D expenditure, along with well-structured records, can support a clear distinction between development activity and income gained from patented innovation.

What data needs to be collected for an R&D and Patent Box claim?

An R&D tax relief claim requires the collection of both technical and financial information that reflects the qualifying activity undertaken during the project development process.

For an R&D tax relief claim, the claimant is required to submit detailed technical and financial documentation to HMRC. The documentation includes technical narratives describing how scientific or technological uncertainties were addressed, along with detailed records of eligible expenditure such as staffing costs, subcontractors and consumables. Companies are also required to submit an Additional Information Form (AIF), and in some cases a Claim Notification Form (CNF), depending on the circumstances of the R&D tax credit claim.

For Patent Box relief, the process is different to R&D tax relief. At a high level, it applies to profits attributable to patented inventions and requires alignment between those profits and the relevant intellectual property (IP).

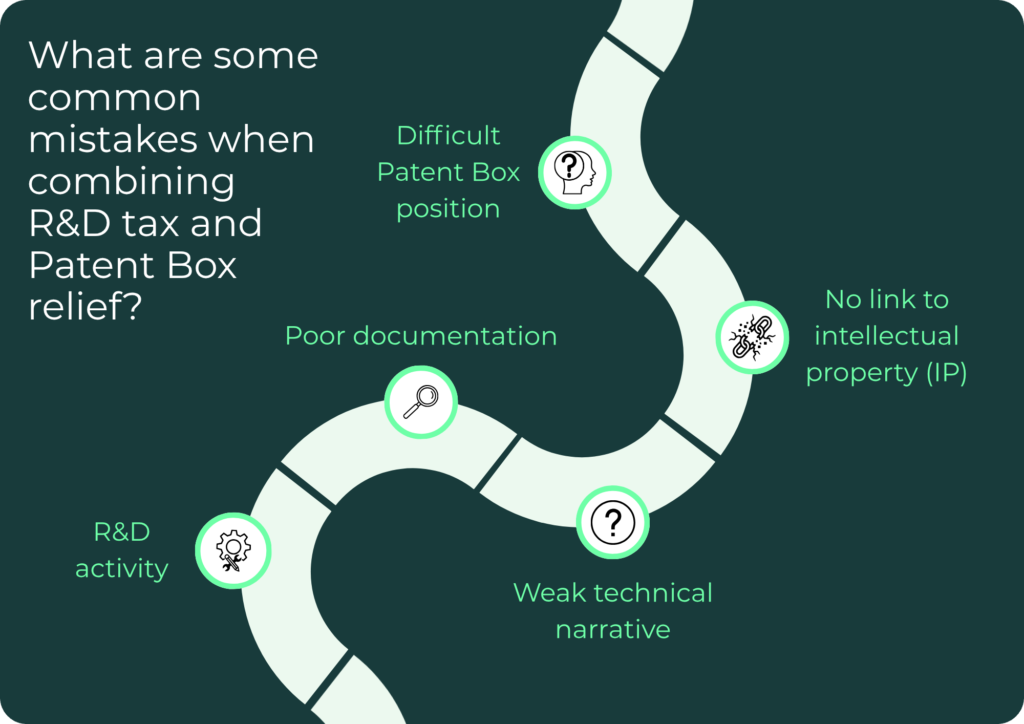

What are some common mistakes when combining R&D tax and Patent Box relief?

Where R&D tax relief and Patent Box both apply, the treatment of qualifying activity and income generated from patented innovation differs under each regime. While both can apply to the same underlying innovation, issues can arise where R&D tax relief claims are prepared without considering how that activity links to income attributable to patented inventions.

Where Patent Box is also applicable, a lack of alignment between R&D documentation and intellectual property (IP) can create difficulties in supporting the overall tax position for the business. This is particularly relevant where development activity has contributed to the creation of patented innovation. Clear and consistent technical records can help demonstrate how qualifying activity relates to those outcomes.

With R&D tax relief, the focus is on ensuring that claims are based on well-documented technical evidence, supported by a competent professional, and aligned with HMRC guidance. Clear and consistent record-keeping is a key aspect of a claim, particularly where the outcome of that R&D activity may later be linked to patented innovation. This helps ensure that qualifying activity is clearly evidenced and can be supported if reviewed.

How is Patent Box relief relevant to R&D tax relief?

Patent Box and R&D tax relief apply at different stages of the innovation lifecycle.

Where R&D tax relief supports qualifying activity and eligible expenditure during development, Patent Box applies a reduced rate of Corporation Tax to profits generated from patented inventions once they are commercialised.

While both types of relief can relate to the same underlying innovation, they operate as separate regimes with different eligibility criteria.

What are the benefits of Patent Box and R&D tax relief?

Each type of relief has their benefits, they are both powerful UK tax incentives designed to support businesses through the innovation process.

Some of the benefits of R&D tax relief include support for loss-making SMEs, being able to reinvest tax savings into future innovative R&D projects and a cost reduction. This can improve cash flow during the research and development phase and enable businesses to reinvest into further qualifying R&D activity.

Some of the benefits of Patent Box relief include support with the commercialisation of intellectual property, a lower Corporation Tax rate and unlocks an advantageous competitive edge.

Closing thoughts: How can Alexander Clifford help with claiming R&D tax relief?

At Alexander Clifford, we support UK businesses in preparing R&D tax relief claims across a range of sectors. While Patent Box relief isn’t something we can help with at this time, we do support companies with identifying qualifying R&D activity, assessing eligible expenditure, and ensuring each submission aligns with HMRC’s criteria. We focus on producing clear, evidence-based R&D tax relief claims that can withstand an enquiry.

Following a successful R&D claim, we can help identify whether there may be an opportunity to benefit from Patent Box and guide you on the next steps to explore this further. If you would like to discuss an R&D tax relief claim, you can get in touch with our team.