What is an HMRC R&D tax credit enquiry?

An HMRC R&D tax credit enquiry is a formal investigation HMRC uses to assess if the expenditure and activities in your claim qualify for tax relief. HMRC have toughened compliance measures after The Office for National Statistics reported that an estimated 4.9% of R&D tax relief payout is attributable to error and fraud.

What’s the history of HMRC internal R&D specialist units?

In 2006, seven HMRC internal R&D specialist units were set up to deal with R&D tax credits claims. Today, compliance is handled by the Individuals & Small Business Compliance (ISBC) and WMBC teams. Large Business cases are managed through HMRC’s Large Business Directorate.

How many enquiries does HMRC raise?

HMRC R&D enquiries have increased, now affecting 17% of all R&D claims. Between 2023 and 2024, this affected 9,700 claims. More staff, and the adoption of AI tools has made it easier for HMRC to check claims more thoroughly.

Why is HMRC’s specialist unit targeting my claim?

If HMRC have opened an enquiry into your R&D claim, it could be deemed as high-risk. This could be caused by a random audit, your company falling into a historically risky category, or an anomaly on your claim.

Facing an R&D enquiry? We’ll defend your claim

What’s the role of the R&D Specialist Unit (Anti-Abuse Unit)?

The R&D Anti-Abuse Unit was created to combat error and fraud with targeted risk profiling and data analytics.HMRC’s AI use can also detect patterns of non-compliance. Each claim is assessed using the BEIS or HMRC guidelines. The Anti-Abuse Unit now handles all complex and high-value R&D claims. HMRC R&D enquiry defence can help you tackle the audit and resolve any questions.

What triggers an HMRC R&D tax credit enquiry?

Since August 2023, HMRC has required all R&D claims to be accompanied by an Additional Information Form (AIF). Incomplete, vague, or overly technical submissions can trigger an HMRC R&D tax credit enquiry.

Other risk indicators:

- Mismatches between your SIC code and the type of R&D claimed

- Being in a high-risk sector

- Repeatedly high claim percentages over multiple years

- Disproportionately large claims relative to company size

What are the statutory time limits for R&D enquiries?

Under paragraph 24 of the Finance Act 1998, HMRC 12 months from the file date to open HMRC internal R&D specialist units enquiries. Resubmission or amendment restarts the clock, extending the HMRC R&D tax credit enquiry window. You may be able to amend errors during your HMRC R&D enquiry defence, but later changes can expose you to further investigation.

What are the different types of specialist R&D units, and what’s the best approach?

- Individuals and small business compliance (ISBC) – ISBC’s Campaigns & Projects team runs high-volume R&D checks. Your enquiry will be processed quickly and efficiently, but HMRC mistakes can happen

- Wealthy and mid-sized business compliance (WMBC) – Enquiries are selected using random sampling. Your identified risks may be questioned via video call. Cooperation and clear evidence are key to resolution

- Large business (LB) – Usually, businesses seek the help of an R&D specialist who will work with your business and HMRC. Your CCM should contribute to a staged plan with agreed timelines and ongoing dialogue

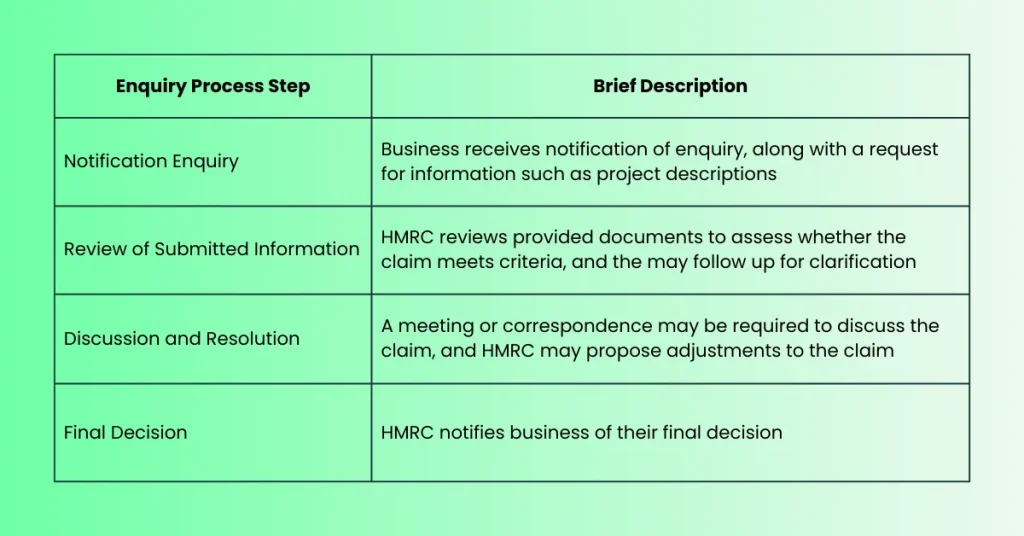

How do I respond to R&D specialist units enquiries?

You can respond to HMRC R&D enquiries through the alternative dispute resolution (ADR) process, or by tribunal. HMRC will offer a closure notice once all questions have been cleared up.

Provide a technical counter-argument

Once an HMRC R&D tax credit enquiry begins, it’s important to respond with competence, precision, and transparency.

Evidence CIRDD81900 criteria

HMRC’s internal guidance (CIRDD81900) outlines four key tests every R&D project must meet. It’s important to defend HMRC internal R&D specialist units enquiries by proving that you fulfil this criteria:

- Advance in science or technology – Show that your project sought to improve industry knowledge, not just your business

- Scientific or technological uncertainty – Define the obstacles that couldn’t be resolved through standard practice

- Competent professional – Identify the expert who led or validated the R&D process and evidence their qualifications

- Systematic and investigative process – Prove you followed a structured methodology, with trials, tests, or iterations

Document your finances

An HMRC R&D tax credit enquiry often challenges the accuracy of cost apportionments. HMRC expects a clear link between each cost and the qualifying R&D activity. Offer evidence when defending HMRC internal R&D specialist units enquiries such as:

- Timesheets and project logs – Show how employee time was split between qualifying and non-qualifying activities

- Apportionment methodology – Demonstrate fairness and reasonableness

- Records of Externally Provided Workers (EPWs) – Include invoices and statements of work

Complex cases involving subcontracted work or overseas R&D expenditure require additional clarity, as HMRC is particularly focused on these costs.

How do I navigate HMRC R&D enquiry defence? Resolution, penalties, and appeals

If your HMRC R&D enquiry defence doesn’t satisfy HMRC, the case may escalate. Each round of correspondence in HMRC R&D enquiry defence must be addressed carefully. Avoid emotional or defensive language.

Manage correspondence and request a closure notice

Avoid emotional or defensive language. If you’ve provided all evidence requested, you can formally request a closure notice under Section 28A of the Taxes Management Act 1970. This will either end the HMRC R&D tax credit enquiry, or prompt HMRC to specify what remains unresolved – a key tactical move in many R&D tax credit enquiry resolution service cases.

Penalty mitigation – ‘Telling, Helping, Giving’

If HMRC spots an error, penalties may apply. The severity depends on whether the mistake was general, careless, or deliberate. Using the ‘Telling, Helping, and Giving’ framework in your HMRC R&D enquiry defence can reduce penalties significantly:

- Telling – Voluntarily informing HMRC of an error before they find it

- Helping – Cooperating fully during the HMRC enquiry into your R&D claim

- Giving – Providing all relevant documentation promptly

Final options

If you disagree with HMRC’s final decision, several HMRC R&D enquiry defence appeal routes exist:

- Statutory review – A different HMRC officer re-examines the decision

- Alternative Dispute Resolution (ADR) – Mediation that can avoid unnecessary costs

- First-tier tribunal – A formal appeal process, where evidence and expert testimony can be presented

What are the outcomes of an HMRC enquiry?

HMRC will offer a final outcome for your HMRC R&D tax credit enquiry – approval, amendment or rejection. They may issue a penalty after the rejection. Using an R&D tax credit enquiry resolution service can give you the best chances of a successful outcome.

Alexander Clifford specialise in representing clients during HMRC R&D enquiries and defending claims before HMRC’s R&D Specialist Units. Our HMRC R&D enquiry defence service includes:

- A detailed review of all correspondence, claim documents, and AIF submissions

- Preparation of robust technical and financial counter-arguments

- Direct communication with HMRC to expedite resolution

Whether your business operates under the RDEC Scheme or the SME framework, reach out to find out how our R&D tax credit enquiry resolution service can protect legitimate innovation funding, and prevent future compliance issues.

HMRC enquiries into R&D claims – FAQs

How long does an HMRC R&D enquiry last?

R&D enquiries are launched by HMRC to assess whether your claim is eligible for relief. Most enquiries last between three and six months, though complex cases handled by R&D Specialist Units enquiry teams can extend up to a year.

Can HMRC open an enquiry after I’ve received tax credits?

Yes. HMRC can open an enquiry into an R&D claim within 12 months of submission, even if payment has already been made. Consider seeking help from a specialist R&D tax credit enquiry resolution service.

What are the penalties for an incorrect R&D tax credit claim?

Penalties range from 0% to 100% of the tax credits, depending on whether the error is accidental or deliberate. Honest cooperation in your HMRC R&D enquiry defence can significantly reduce liability.

What’s the difference between a statutory review and an appeal?

A statutory review involves a new internal HMRC officer reassessing your case, while an appeal is an independent judicial process made directly to the tribunal. R&D specialist units enquiries can be resolved through either of these avenues.

Can HMRC reject my claim without an enquiry?

Yes, HMRC can reject your R&D claim without an enquiry. This could be because you didn’t notify them in time, you didn’t submit an AIF, or you didn’t include some vital information.

Get a decision on your R&D eligibility from a qualified specialist in 15 minutes.